In mid-2025, ALG published its whitepaper “Logistics at a crossroads: a shifting scenario, Economic Zones, and Africa's potential”, exploring the challenges facing the logistics sector, the potential role of Economic Zones, and the emerging position of Africa within global supply chains. The paper generated strong interest across industry stakeholders, as it captured a moment in which global logistics was entering a phase of profound uncertainty and transformation.

Yet, the context has not remained static. Over the past 12–18 months, many of the dynamics identified in the original analysis have not only persisted, but intensified. Geopolitical tensions have continued to reshape trade flows, cost structures have become increasingly volatile, and companies have begun to take more structural decisions regarding the reconfiguration of their supply chains.

Against this backdrop, revisiting these reflections becomes particularly relevant, not simply to update the analysis, but as an opportunity to reassess how these dynamics are evolving and what they imply for the future of the logistics sector.

Building on recent developments and ALG’s ongoing work across logistics ecosystems, this article examines the evolving global supply chain landscape, the structural forces shaping the sector, and the role Economic Zones may play, with a particular focus on Africa as an emerging actor.

Global logistics under pressure: a changing landscape

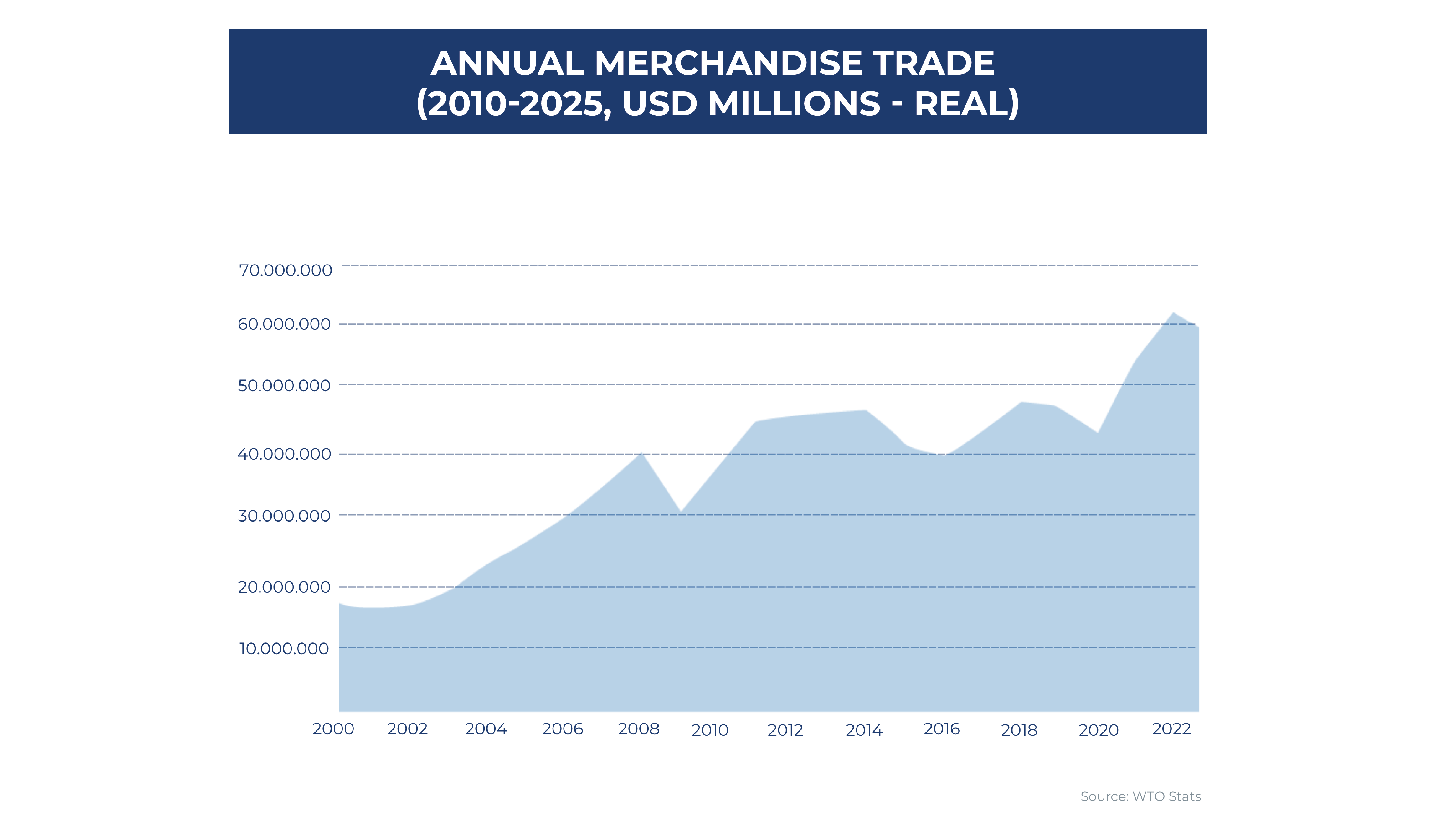

The macroeconomic environment confronting the logistics sector has shifted markedly since the post-pandemic rebound. Following years of strong growth, global merchandise trade contracted in real terms in 2023, marking a shift in the upward trend. While exports rebounded sharply in 2021, growth has since stabilized and is expected to remain moderate in the medium term, albeit with an increasingly uneven distribution across regions and sectors.

This asymmetry reflects a broader fragmentation of global trade. Geopolitical tensions, including tariffs, supply chain disruptions, and security risks, are reshaping traditional trade configurations, fostering regional clustering and supplier diversification.

At the same time, logistics cost structures have become increasingly exposed to volatility in energy markets. Fuel costs, particularly bunker fuel in maritime transport, which can account for up to 50–60% of operating costs, remain highly sensitive to geopolitical developments. Recent disruptions in key routes, such as the Strait of Hormuz in early 2026, have further illustrated how localized events can have global implications on logistics pricing and availability.

This volatility is already being reflected in port-level dynamics, where fuel shortages and supply constraints have translated into sharp increases in bunker premiums and operational costs at key hubs. Episodes such as the surge in very-low-sulphur fuel oil (VLSFO) prices in ports like Fujairah (USD 50/ton vs. averages of USD 15/ton for April 2026 as per market data) highlight how disruptions at specific locations can quickly cascade across global shipping networks, affecting freight rates and overall logistics costs.

In parallel, demand patterns have also become more volatile. Anticipatory behavior from businesses, such as frontloading imports ahead of potential tariff changes, has led to uneven demand patterns, combining peaks of activity with subsequent slowdowns. The result is a more complex and less predictable logistics environment.

In such a context, companies are increasingly reassessing their sourcing strategies. Concepts such as nearshoring, reshoring, and “China +1” have evolved from contingency considerations into long-term strategic priorities aimed at enhancing resilience and reducing exposure to global disruptions. This term, “China +1”, refers to the diversification of global manufacturing footprints by adding alternative production locations beyond China, enabling companies to reduce risk and optimize costs while maintaining a presence in the Chinese market.

Together, these approaches illustrate a broader shift: rather than optimizing solely for cost, companies are redesigning their supply chains to strike a balance between efficiency and resilience in an increasingly fragmented global trade landscape.

Structural challenges facing the logistics sector

Beyond macroeconomic shifts, the logistics sector continues to face a set of structural challenges that are shaping its performance.

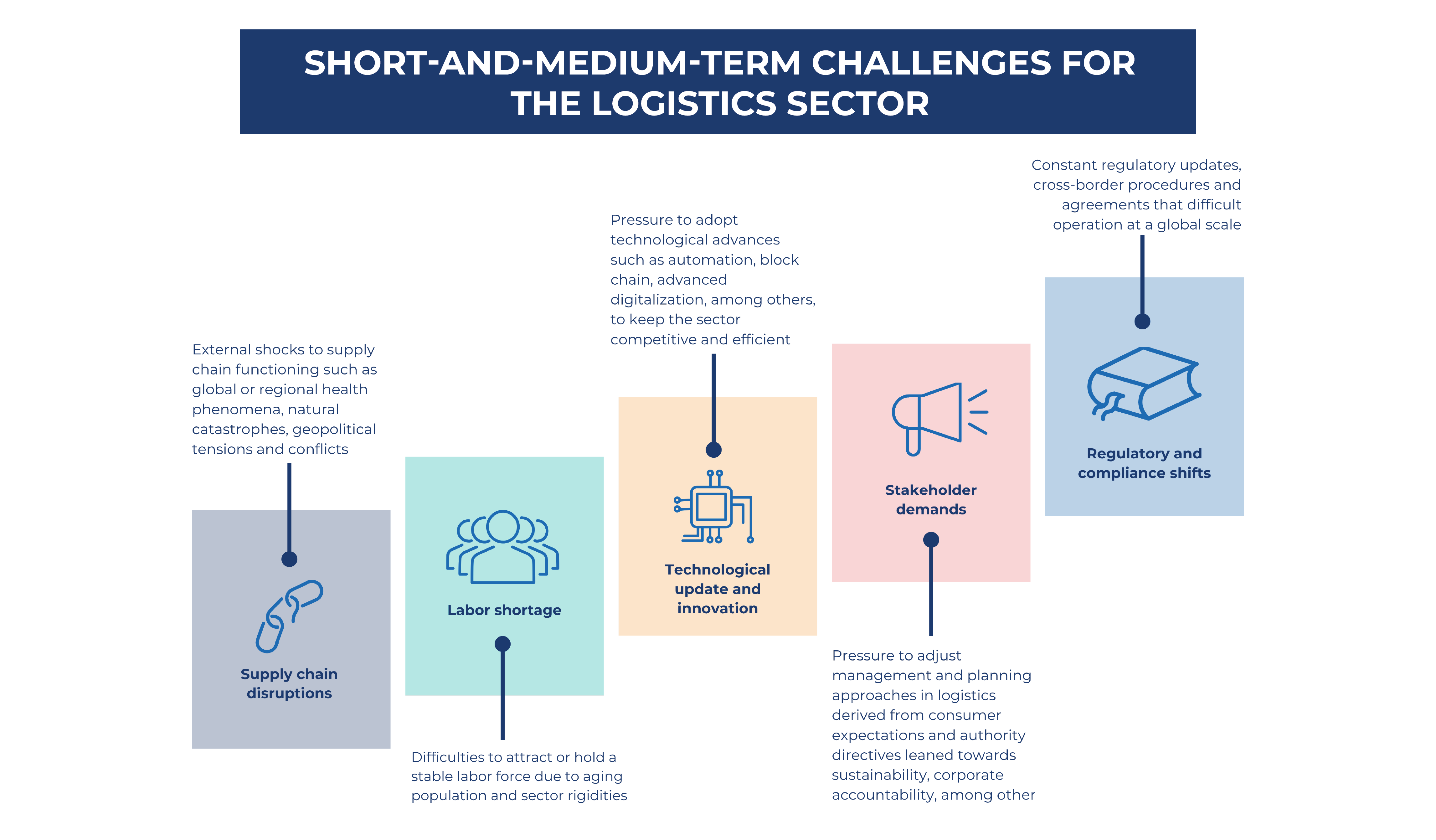

Supply chain disruptions and geopolitical risk have become a persistent feature rather than an exception. Trade disputes, climate-related events, security incidents, and regulatory shifts have contributed to rising uncertainty and cost pressure across global supply chains. Even when disruptions are geographically localized, their impact is amplified through the interconnected nature of global logistics networks.

Freight indices illustrate this volatility, with sharp fluctuations driven by both physical constraints and market expectations. Episodes such as sudden tariff changes or route disruptions can rapidly translate into price spikes or demand shifts, compressing margins for logistics operators.

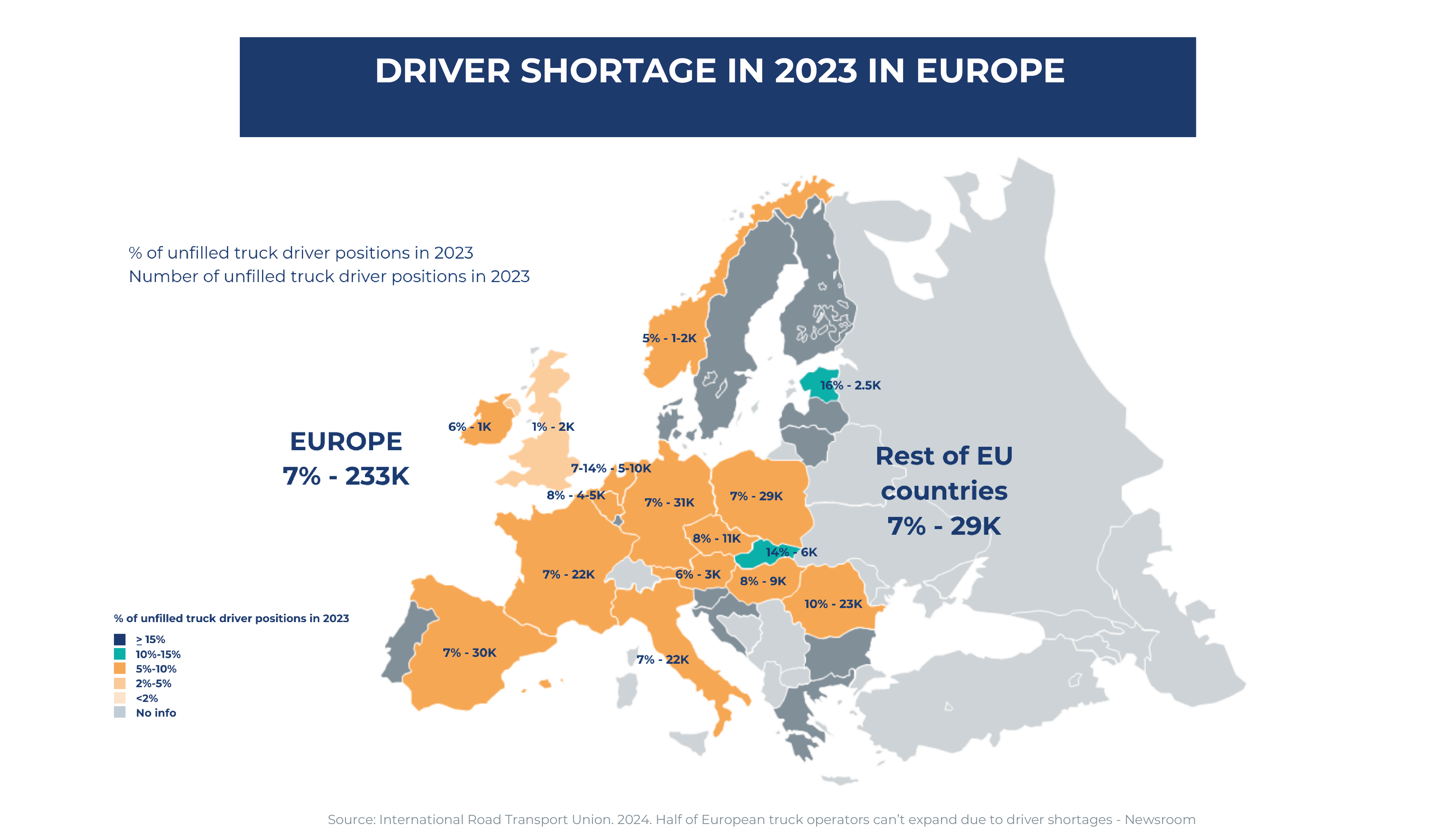

At the same time, labor and skills constraints continue to intensify. The logistics sector, inherently labor-intensive, is particularly exposed to demographic trends such as workforce aging. Shortages of truck drivers, warehouse operators, and specialized personnel have become structural in several regions, limiting capacity expansion and reducing operational flexibility.

Technology and digitalization offer clear opportunities to address some of these pressures. Artificial intelligence, automation, and advanced analytics are increasingly being explored to improve forecasting, optimize inventory, and enhance operational efficiency. However, adoption remains uneven, as implementation requires significant investment, integration efforts, and workforce upskilling.

Finally, sustainability and customer expectations are reshaping the sector’s priorities. Regulatory pressures towards decarbonization are increasing compliance requirements, while the growth of e-commerce continues to raise expectations regarding the speed and reliability of delivery. As same-day and next-day delivery become standard benchmarks, logistics networks, particularly in urban environments, are under increasing strain to balance service levels, cost efficiency, and environmental performance.

Economic zones as enablers of resilience and efficiency

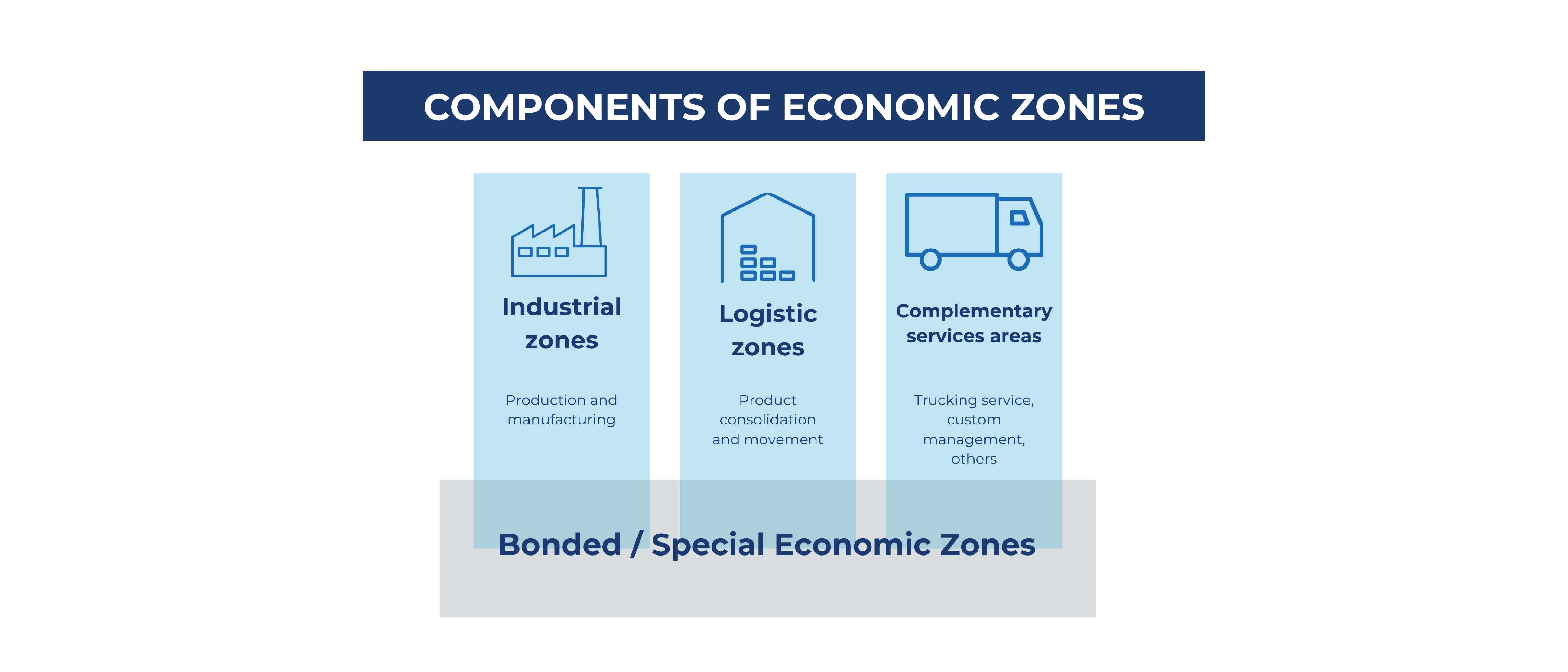

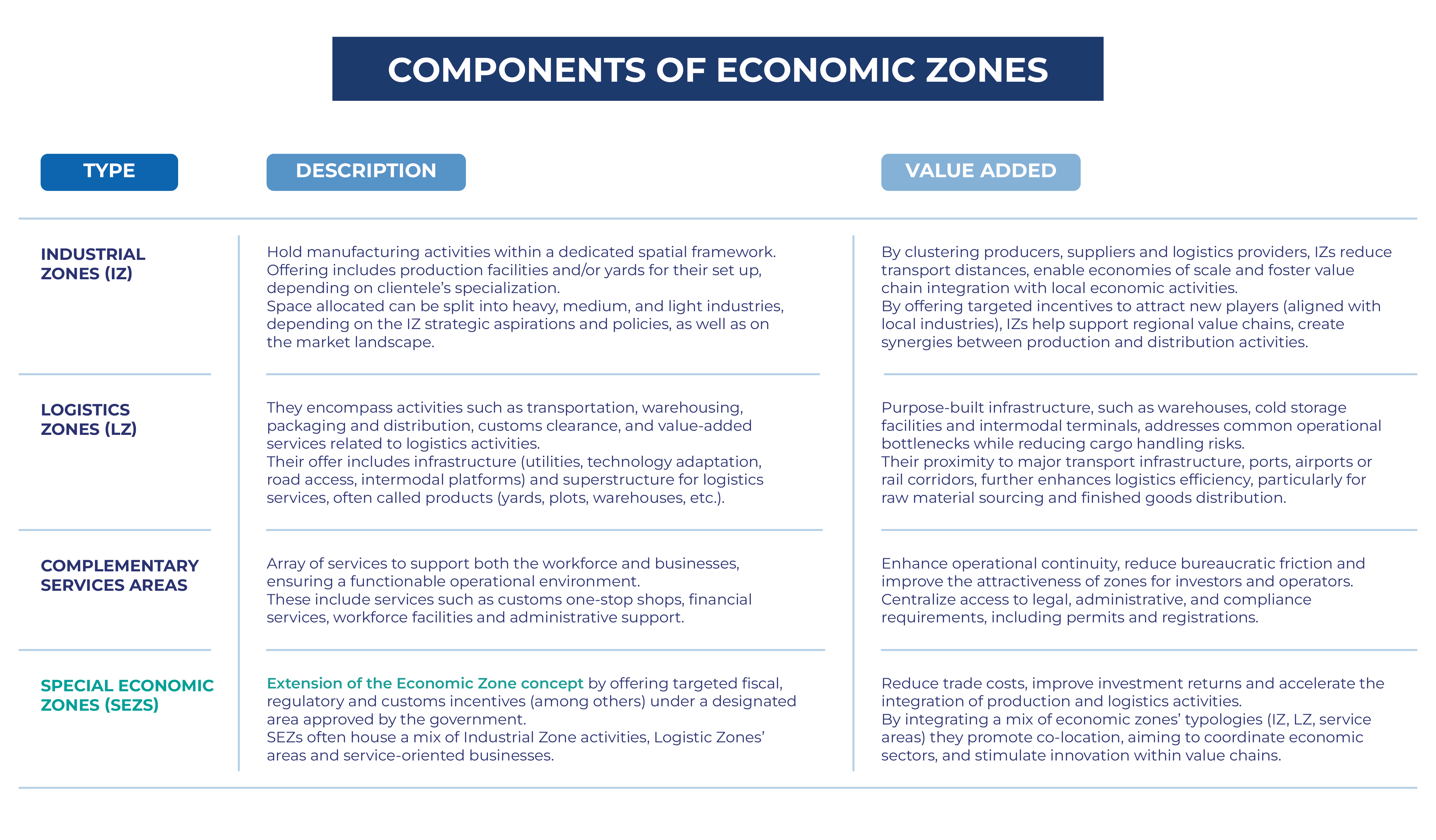

As global supply chains enter a phase of reconfiguration, Economic Zones are gaining renewed relevance as strategic enablers of logistics performance.

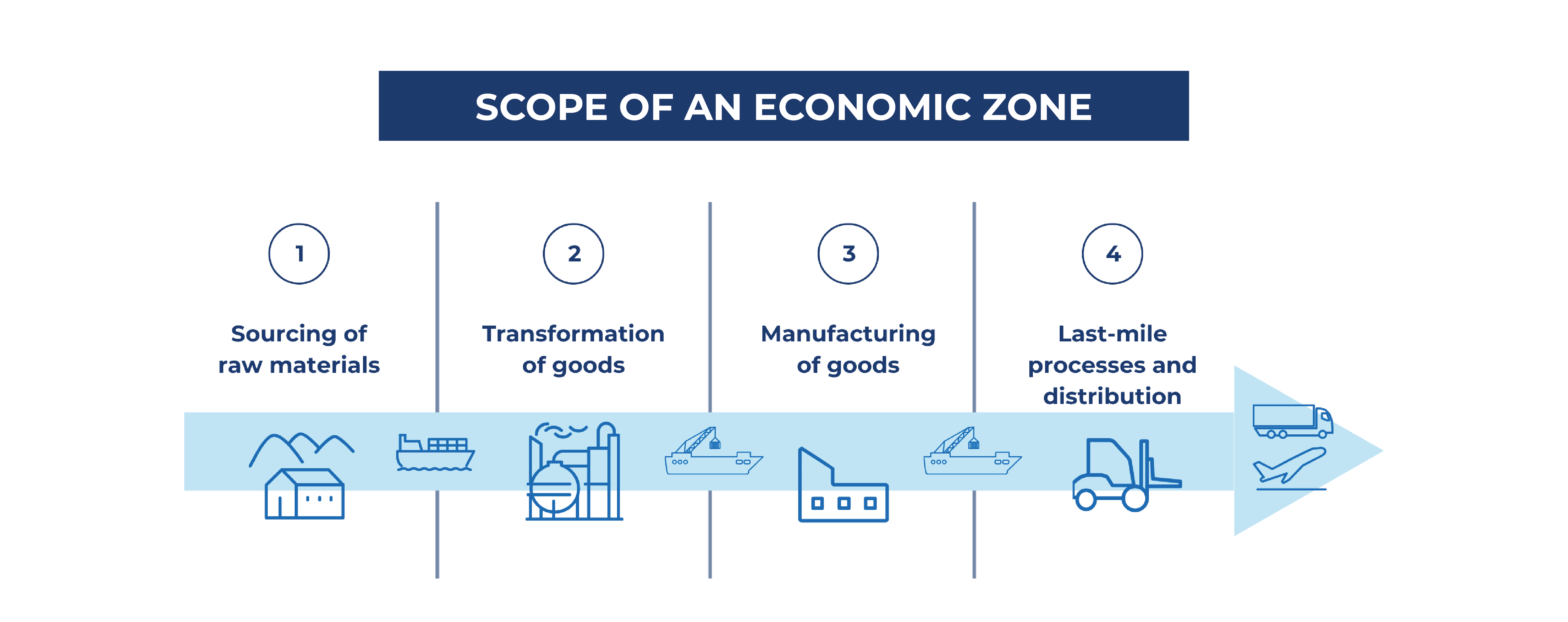

These zones, whether structured as logistics hubs, industrial parks or Special Economic Zones, are designed to concentrate infrastructure, services and regulatory frameworks within a defined geographic area. Their objective is to facilitate the efficient movement of goods and enhance the integration of local value chains into global trade.

Their contribution to logistics performance can be understood through three key mechanisms. First, institutional and regulatory frameworks that streamline administrative processes, simplify customs procedures, and accelerate clearance. Second, strategic location and infrastructure design, often linked to multimodal transport nodes, enable more efficient connectivity. Third, economic and service clustering, creating ecosystems where logistics providers, manufacturers, and support services operate in proximity.

Together, these elements contribute to reducing transit times, lowering operational costs, and improving reliability, all critical factors in an increasingly volatile logistics environment.

The use of Economic Zones has expanded steadily over time, driven by their ability to attract investment, promote exports, and generate synergies with local economies. Within this broader category, Special Economic Zones (SEZs) have played a particularly prominent role by offering targeted fiscal and regulatory incentives to attract strategic industries.

Africa as an emerging logistics and economic zones hub

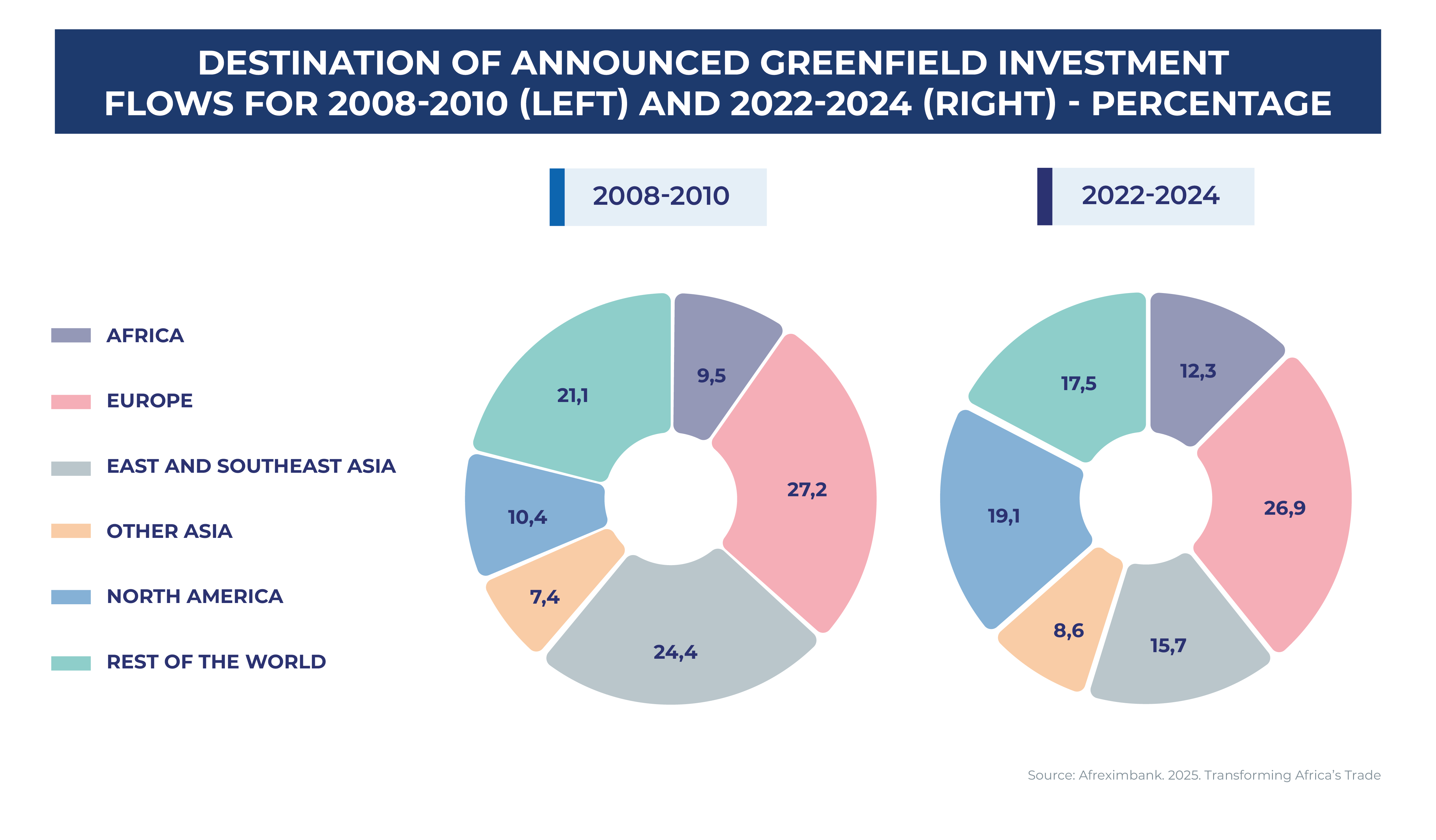

Amid the global reconfiguration of supply chains, Africa is gaining visibility as a potential logistics and industrial partner. The continent’s geographic position, bridging Asia, Europe, and the Americas, combined with the development of regional integration initiatives such as the African Continental Free Trade Area (AfCFTA), creates strong structural advantages. In addition, demographic dynamics, including a young and growing population, provide a potential response to labor shortages affecting other regions.

Several African economies have experienced sustained economic growth in recent years, accompanied in some cases by reforms aimed at improving investment conditions. This has contributed to increasing Africa’s attractiveness as a destination for greenfield investment.

At the same time, the expansion of industrial zones, logistics hubs, and SEZs reflects a growing effort to position the continent within global value chains. Examples such as industrial parks in Ethiopia, logistics platforms linked to major ports such as Tanger Med, or large-scale free zones in Djibouti illustrate the diversity and ambition of these developments.

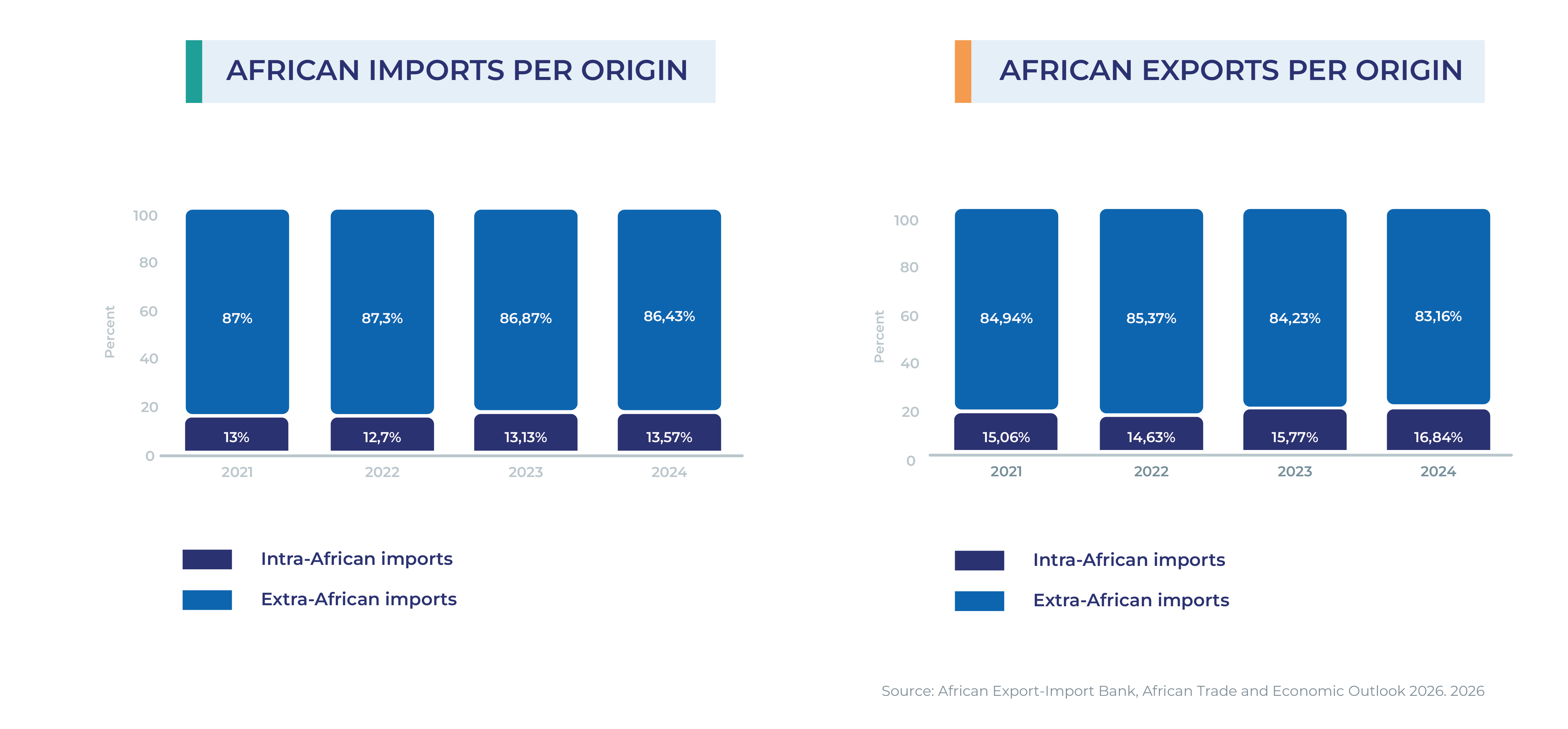

However, Africa’s participation in global trade remains relatively limited, and its industrial base continues to be dominated by resource-driven activities or low-to-medium value-added manufacturing. Regionally, there’s a constant stagnation and lack of integration among African countries, where intra-African imports have not reached 14% of total African countries’ imports in the past years and intra-African exports just represent, nowadays, less than 17% of total African exports (As per Afreximbank trade estimates for 2025). These conditions represent both a constraint and an opportunity.

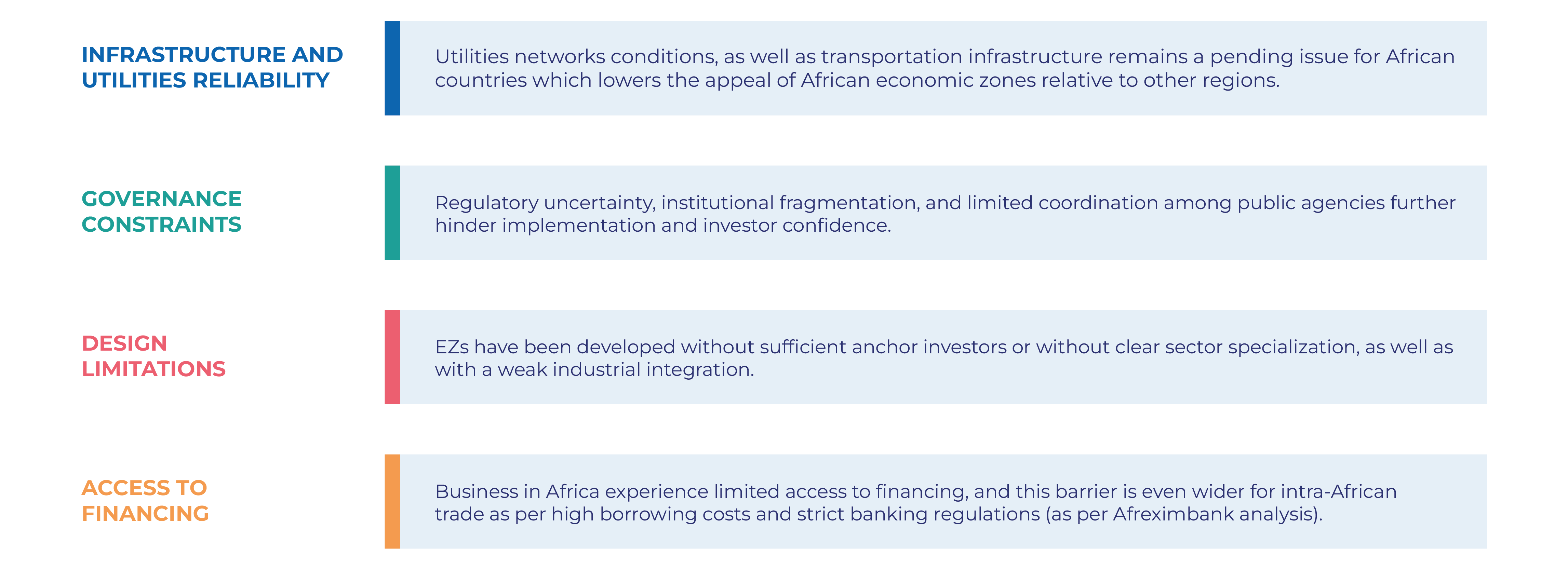

A critical factor is that investors are increasingly prioritizing operational reliability over cost considerations alone. Infrastructure quality, customs efficiency, regulatory predictability, and access to services are key variables in investment decisions, and in many cases, these remain areas for improvement across the continent.

Consequently, while the opportunity for Africa is real, it is also conditioned. The most successful experiences to date suggest that performance depends less on incentives and more on the quality of execution: specialization, integration with logistics corridors, and alignment with market demand.

Outlook and strategic implications from ALG standpoint

Global supply chains are undergoing a structural reconfiguration. Fragmentation, regionalization, and risk diversification are reshaping how logistics networks are designed and operated, while cost volatility and operational uncertainty continue to redefine performance benchmarks across the sector.

From ALG’s experience working with public institutions, logistics operators, and Economic Zone developers, these shifts are already translating into tangible decisions. Clients are increasingly prioritizing resilience over cost optimization, reassessing their geographic footprint and looking for integrated solutions that combine infrastructure, connectivity, and regulatory efficiency.

At the same time, we observe growing interest in Economic Zones as strategic platforms, not only to attract investment, but to enable more robust and adaptable supply chains. However, this interest is also accompanied by greater scrutiny: investors and operators are no longer evaluating zones based solely on incentives, but on their ability to deliver operational reliability, integration, and long-term performance. Against this backdrop, several key reflections emerge:

- Economic Zones are transitioning from policy instruments to critical infrastructure within global supply chains. Their relevance will depend not on their scale, but on their specialization, execution capacity, and integration with logistics corridors and value chains.

- Competition for investment is intensifying. Countries and regions are no longer competing on cost alone, but on their ability to provide stable, predictable, and efficient operating environments.

- Africa’s opportunity is real, but inherently selective. The continent is well positioned to benefit from global trends such as “China +1” or supply chain diversification, yet success will depend on addressing fundamental challenges related to infrastructure, governance, and execution. The experience of leading zones shows that performance is driven by focus, integration, and alignment with market demand.

Ultimately, the current transformation of global logistics is not about replacing existing hubs, but about redefining how and where value is created within supply chains.

In this context, ALG supports clients in navigating this complexity, from defining strategic positioning to designing and implementing logistics and Economic Zone solutions. By combining sector expertise with on-the-ground experience, ALG helps stakeholders translate global trends into actionable, sustainable, and competitive projects.

About the authors

Joan Miquel Vilardell

PhD and MSc in Civil Engineering, and holds an MBA. Partner at ALG. Global Logistics Lead & Head of Africa Business.

Daniel Gordo Garzón

MBA and M.A in Economics, Senior Consultant at ALG, with focus on infrastructure and logistics projects in Africa.

– A key to future competition in businesses that are heavily dependent on supply chains")

")