Global trade is a major driver of greenhouse gas emissions, accounting for approximately 7% of global CO2 emissions. Maritime transport logically plays a central role in this footprint, as it carries nearly 80% of global trade volumes. Consequently, it has become a focal point of global climate commitments and decarbonization efforts. Initiatives such as Green Shipping Corridors, launched at COP26 in 2021, aim to create cleaner maritime routes through low carbon vessels, alternative fuels, and greener port operations.

However, this growing attention hides a fundamental paradox: the maritime leg represents only a fraction of the door to door logistics chain and, despite representing the shortest fraction, the inland leg often accounts for about 50% of total costs and emissions. At a global scale, maritime trade represents only about 2-3% of emissions, with the remaining 4% being composed of hinterland transport emissions.

Consequently, to deliver real climate outcomes and materially reduce emissions of global supply chains, decarbonization must extend beyond the port gate. This requires deliberate intervention in inland transport system, including scaling lower-carbon options and creating the market conditions that enable a strategic, demand-driven modal shift toward greener hinterland solutions.

Railway transport: the key enabler to decarbonize and enhance hinterland transport

The inland segment of global supply chains can be served by road, rail, or inland waterways, but in most regions, the real modal choice comes down to road vs. rail. Among these, rail uniquely combines the characteristics needed to not only decarbonize the hinterland but also to expand it and optimize it.

- Rail emits up to 90% less CO₂ per ton-kilometer than road, making it the most effective lever for reducing the inland share of supply‑chain emissions.

- Rail corridors move large, predictable volumes with far greater efficiency than roads. For ports seeking to expand or defend market share, rail offers a structural competitive advantage.

- When integrated with inland terminals and logistics zones, rail corridors can act as extensions of the port itself. These nodes facilitate consolidation, deconsolidation, and value‑added services, effectively pushing the port’s operational frontier inland and enabling ports to compete in regions far beyond their natural catchment.

In essence, rail simultaneously enables deep hinterland expansion, scalation of traffic flows, and delivers meaningful decarbonization. However, unlocking these benefits requires meeting shippers’ two decisive criteria: cost and service quality.

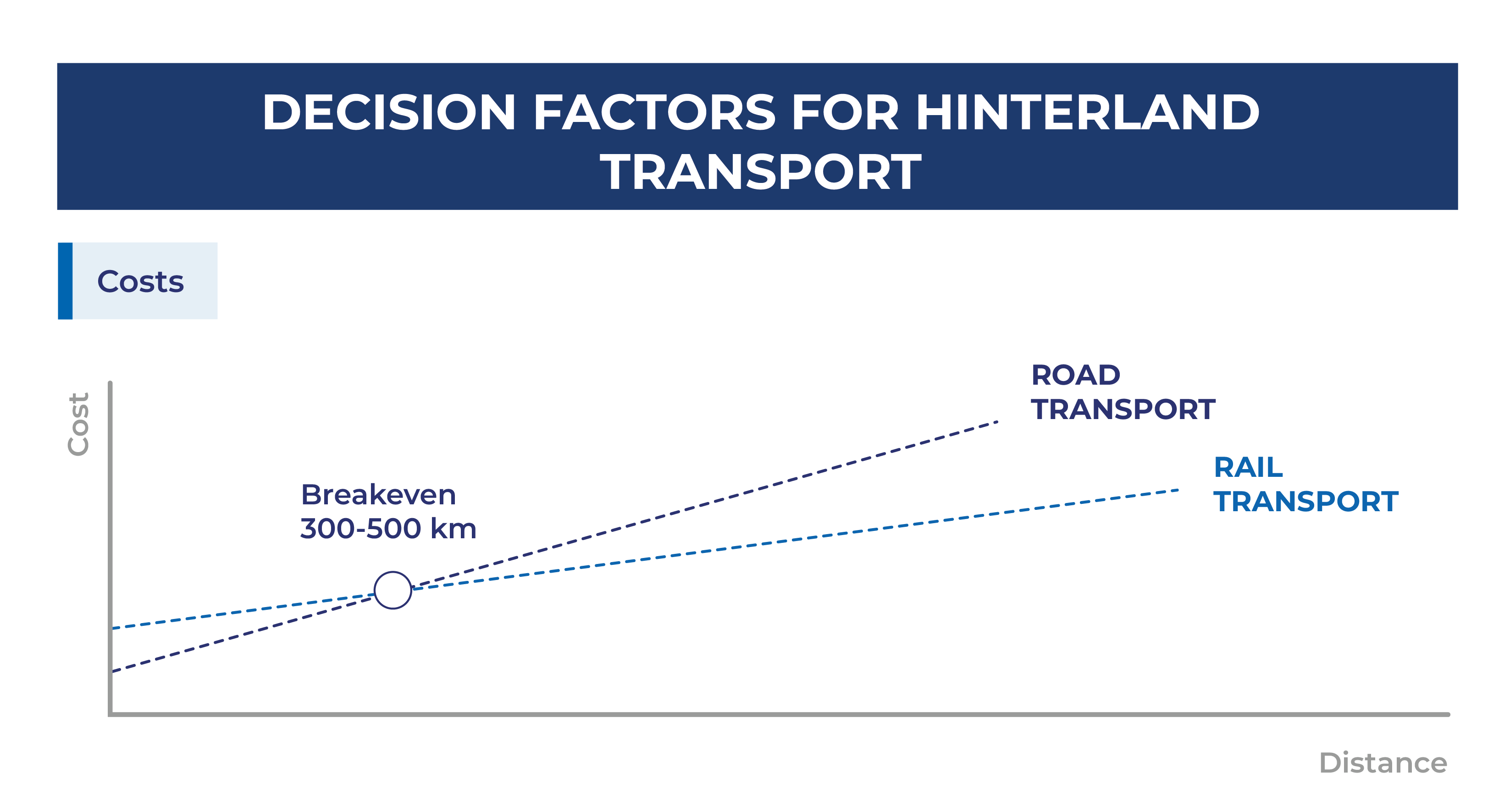

- Cost: While trucks dominate short hauls, rail typically reaches cost parity and then outperforms road beyond 300–500 km, once economies of scale are achieved. Cost is also dependent on the volume of freight, as a critical mass of freight volumes is required to achieve competitive cost levels in railway corridors. For large volumes and bulk transport, rail may even reach breakeven at shorter distances.

- Service quality: Shippers demand reliability, frequency, and predictable transit times. This hinges on efficient operations, robust last mile connectivity, and timely, accurate information flows across the chain. Because rail rarely reaches final destinations directly, well-designed intermodal interfaces and last mile solutions are essential to ensure the competitiveness of rail-based logistics.

When rail delivers on cost and service expectations, hinterland strategies flourish and allow for transport decarbonization. Around the world, ports that have scaled rail effectively have done so by building networks that meet these conditions, enabling them not only to decarbonize inland transport but also to extend their market reach and increase overall throughput.

When rail delivers on cost and service expectations, hinterland strategies flourish and allow for transport decarbonization. Around the world, ports that have scaled rail effectively have done so by building networks that meet these conditions, enabling them not only to decarbonize inland transport but also to extend their market reach and increase overall throughput.

The following three cases illustrate different models through which green rail-based corridors have expanded and optimized a port’s hinterland at different rates of success.

Global cases of hinterland expansion through rail transport

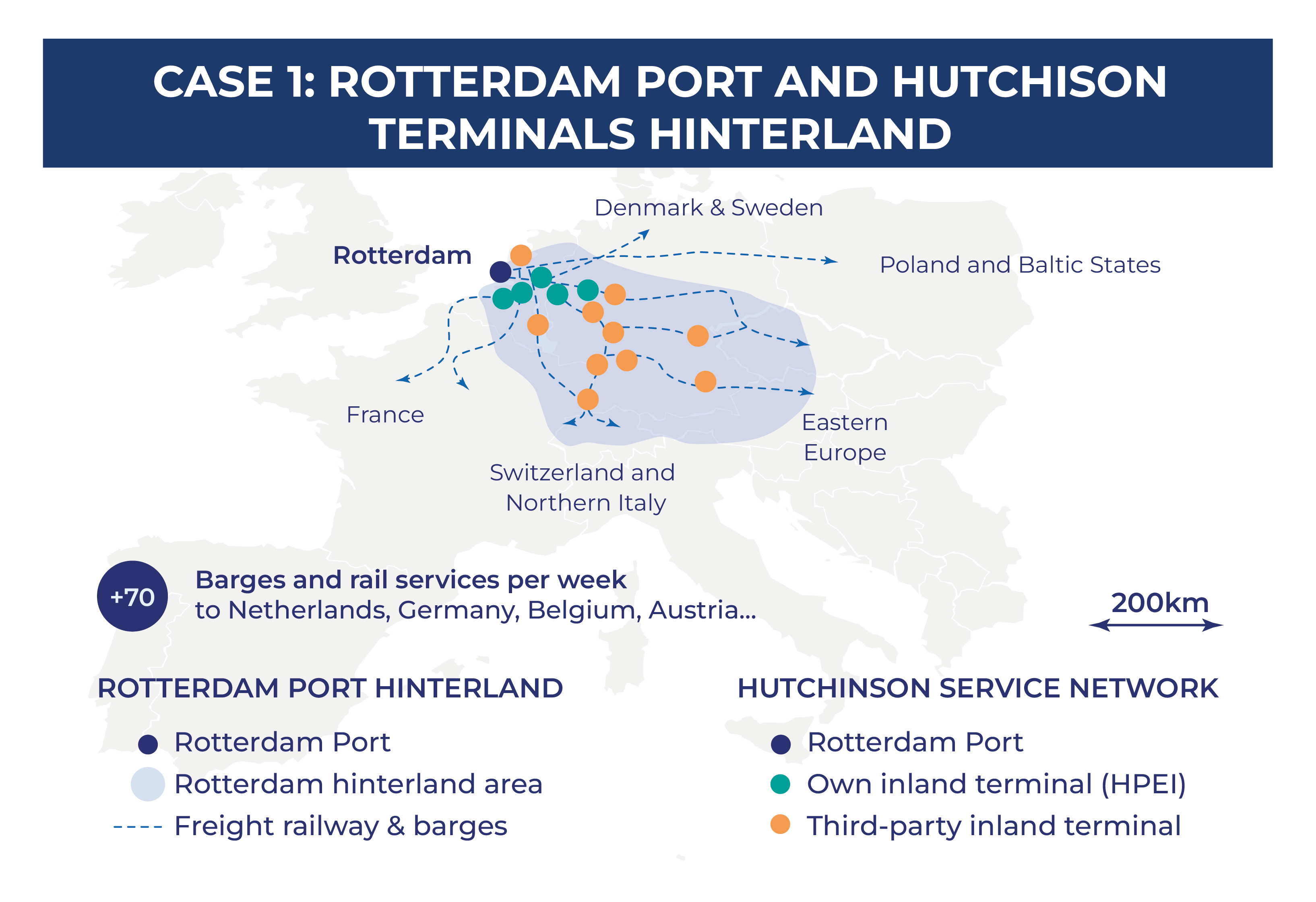

Rotterdam Port and Hutchinson Terminals hinterland

Hutchison Terminals operates as an MTO from the Port of Rotterdam, where it developed a vast service network of inland terminals connected to its semi-automated container terminals at the Port of Rotterdam through dedicated block trains and barges operated by regional operators. From these inland hubs, cargo is distributed to final destinations via coordinated trucking services for last-mile delivery.

Hutchison possesses full control of the intermodal chain, which has not only allowed the company to improve the level of service in overall logistics but also to enhance port operations and become one of the main operators in the port (almost 50% of Port’s container throughput) and region.

Hutchison possesses full control of the intermodal chain, which has not only allowed the company to improve the level of service in overall logistics but also to enhance port operations and become one of the main operators in the port (almost 50% of Port’s container throughput) and region.

On the other hand, their operations are supported by extensive digitalization at the port level, providing real-time data and facilitating communication between stakeholders. This continuously facilitates smooth ship-to-rail transfers, with the Port of Rotterdam claiming up to 20% savings in waiting time.

Thanks to these factors, Rotterdam’s and Hutchison’s hinterland expands over half of Europe, positioning Hutchison’s terminals as the main gateways to the continent.

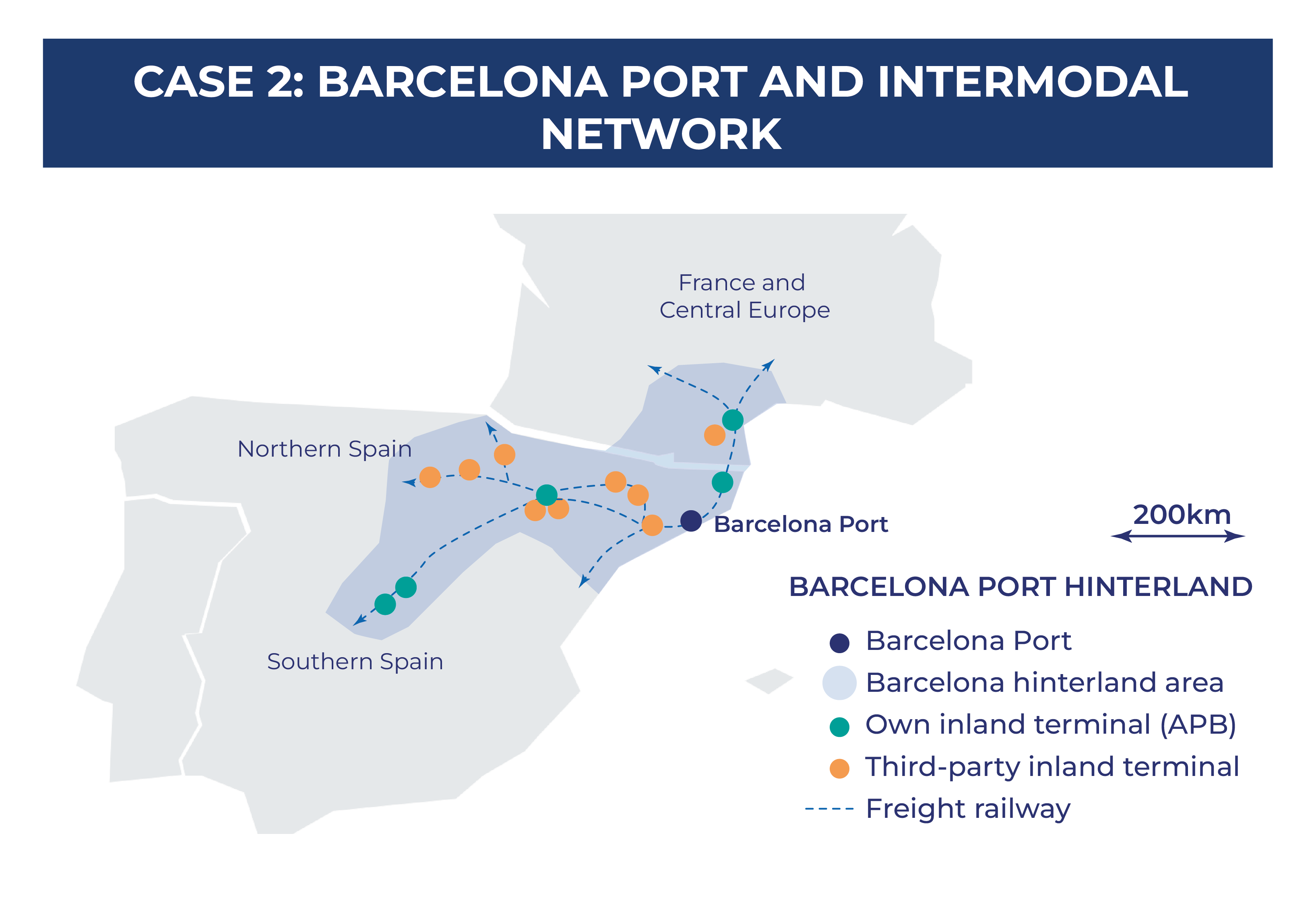

Barcelona Port and intermodal network

The Port of Barcelona includes two semi-automated terminals with an integrated rail marshaling yard operated in conjunction with two private operators.

In its hinterland, the Port participates in several inland depots in key hinterland locations (Zaragoza, France, Madrid…) and holds collaboration agreements with many other third-party terminals. These are served by both truck and rail services coordinated digitally with port and inland terminal operations.

Thanks to its rail network, Barcelona serves an extended hinterland reaching to more than 12 Mn people across Spain, Andorra and France and serving areas that could be otherwise served by other key ports in the region. Particularly, despite its smaller scale and similar distances, Barcelona overcomes Valencia Port as the main Gateway to Aragón province, with over 65% of market share. This is mainly due to its cost-effective hinterland network and its slightly better performance in key indicators (container dwell time and CPPI).

However, there is still room for improvement. The Port’s intermodal network suffers from some unreliability and congestion in the national rail network and limited interoperability with the French network (Iberic vs standard gauge), which limit their level of service and reach into the French hinterland. Moreover, the rail yard currently suffers from operability challenges that limit efficient transfers, but these issues are to be solved with new rail hub at the Port.

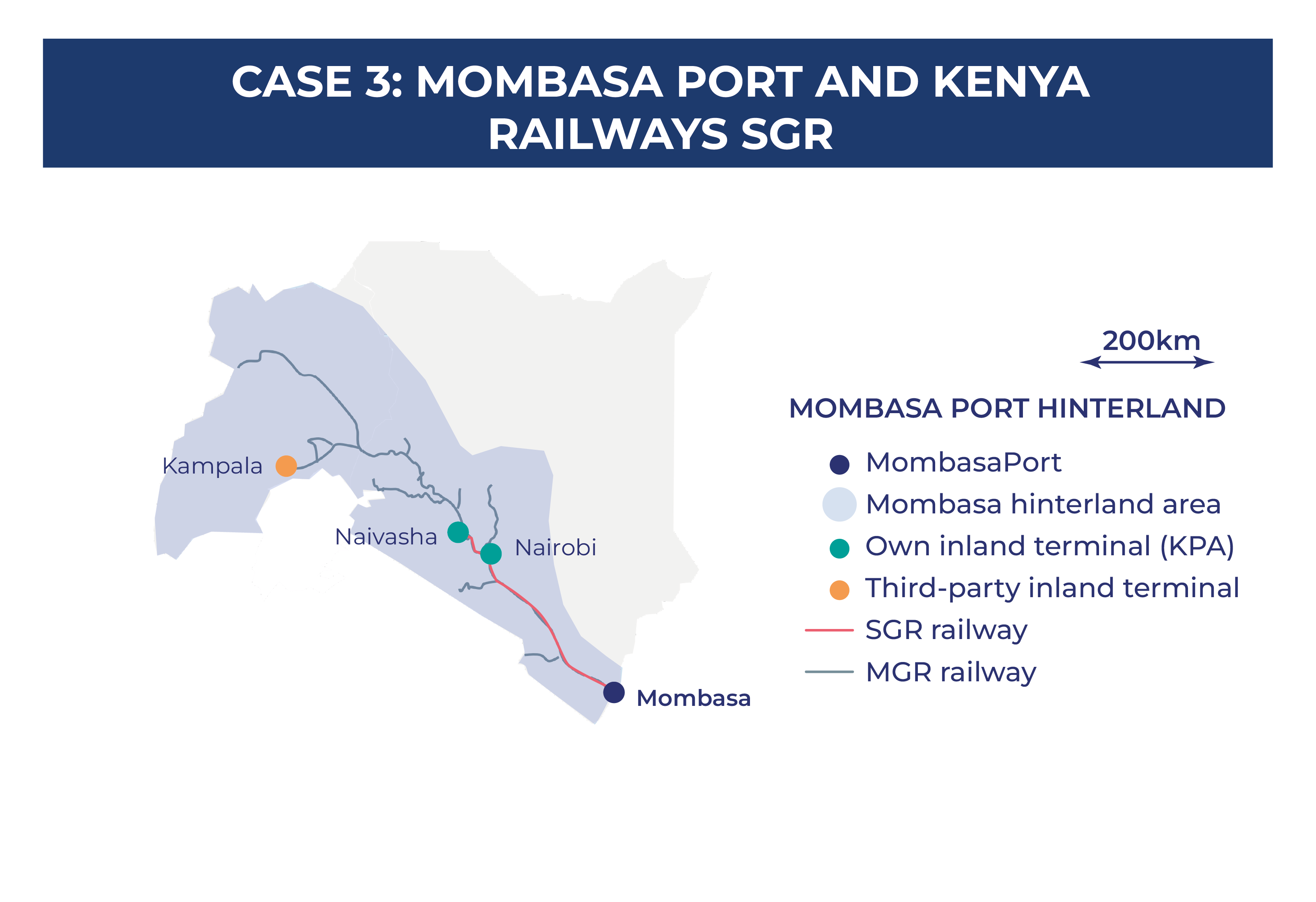

Mombasa Port and Kenya Railways SGR

Kenya Railways developed a modern SGR network as a dedicated port–hinterland rail corridor to connect the Port of Mombasa, the gateway to the region, to the capital Nairobi and rest of the country. The project included an inland terminal at Nairobi and later, another one in Naivasha to serve intermodal transfer for the hinterland, as well as connections to the colonial MGR network to reach further inland.

The network was mainly developed as a state-driven initiative with initially mandated modal shift, not market-driven demand. Costly high last-mile transport and empty return movements have constrained the commercial viability of railway use for transport into the hinterland, particularly for destinations beyond Nairobi. This is compounded by inefficient transshipment processes, limited cargo visibility, and strong competition from the trucking sector, including resistance from well-established road transport operators. As a result, traffic growth has been slower than anticipated, contributing to ongoing financial sustainability concerns, particularly given the project’s substantial debt obligations.

Despite challenges, the railway shifted the modal share of rail from 5% to over 25%, even after non-mandatory use. This shift has led to a meaningful reduction in GHG emissions along the corridor. With this, transit time and reliability along the corridor improved too, along with a slight reduction of informal trucking along the Northern Corridor. The railway also helped to decongest the Mombasa Port and reduce container dwell time.

Key challenges to scaling rail in port hinterlands

Taken together, these three cases illustrate the wide spectrum of outcomes that rail‑based hinterland strategies can deliver. However, they also show that while the potential of rail is significant, success is never automatic and that, in practice, scaling railway solutions within port hinterlands remains challenged by structural barriers. Developing a robust railway network fully integrated into green maritime corridors involves a set of financial, technical, and institutional challenges that often slow or even block implementation.

Many systems suffer from poor interoperability, outdated technical standards, or fragmented institutional arrangements, all of which reduce efficiency and reliability. Some ports still lack on-dock rail access, while others are constrained by small or inefficient marshalling yards, inadequate scheduling, or weak coordination between port authorities and railway undertakings. Further inland terminals and last-mile connections often become bottlenecks, as inefficient transshipment operations or poorly coordinated last-mile links can undermine the reliability of the entire corridor and erode shipper confidence.

Rail also faces strong competition from road transport, which often appears cheaper, faster, and more flexible, particularly in contexts where trucking is under-regulated and does not fully internalize its environmental and social costs. In many regions, powerful road transport lobbies further complicate efforts to rebalance modal shares. Compounding this issue, coordination between rail and road is frequently weak, limiting the effectiveness of intermodal solutions.

Nonetheless, the most significant barrier to rail development is the high level of upfront capital investment required. Beyond construction, operations and maintenance (O&M) costs remain structurally high, while revenue streams tend to materialize gradually as traffic builds up over time. This combination results in long payback periods and elevated risk profiles, increasing the cost of capital and limiting investment appetite.

These challenges explain why, despite clear advantages, rail based hinterland systems are still difficult to scale in many geographies, and why targeted interventions in financing, policy, and governance are essential to unlock their full potential.

Bridging the financial gap in railway development through aligned green financing mechanisms

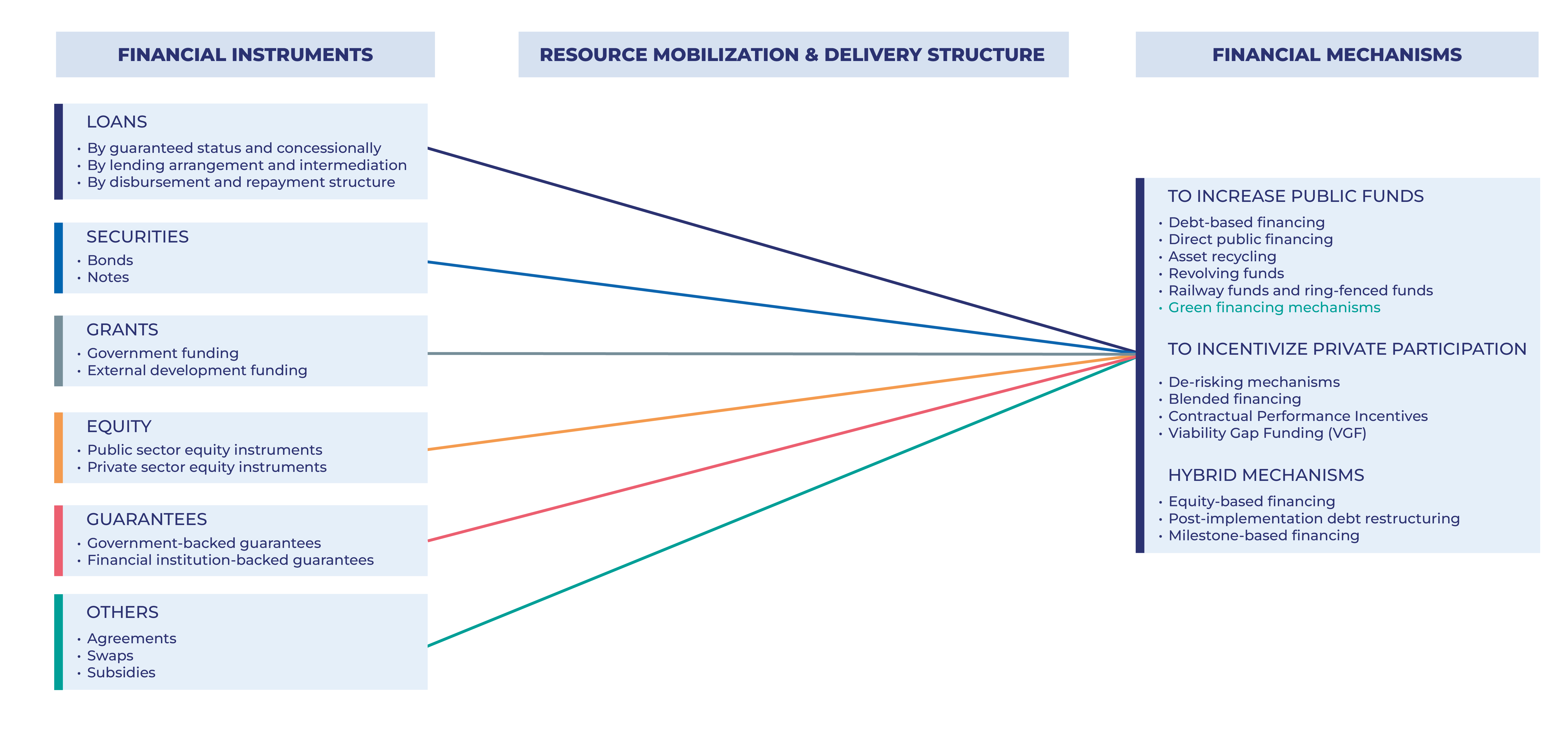

Historically, railway corridor development has relied heavily on public budgets and sovereign borrowing. This approach has often strained national treasuries and constrained the ability of many developing regions to deliver large-scale infrastructure. However, the financing landscape for railway projects, particularly for high-density corridors between ports and their hinterlands, is undergoing significant transformation.

New funding sources are emerging from both public institutions and financial markets, with both governments and private developers are increasingly adopting innovative approaches to mobilize capital and deliver projects, combining different instruments and delivery models in ways that can be mixed and tailored to each project’s specific characteristics, risk profile, and institutional context.

Within this evolving financing environment, green financing is becoming a key lever for raising capital, driven by tighter climate commitments, changing regulatory frameworks, and growing investor demand for sustainable infrastructure assets. Within this space, three main categories of instruments are emerging as particularly relevant:

Within this evolving financing environment, green financing is becoming a key lever for raising capital, driven by tighter climate commitments, changing regulatory frameworks, and growing investor demand for sustainable infrastructure assets. Within this space, three main categories of instruments are emerging as particularly relevant:

- Green bonds: A highly effective and scalable instrument, green bonds are already widely used to finance railway infrastructure in mature markets, such as Germany. In Morocco, the Government also used green bonds to refinance debt incurred for the construction of Africa’s first high speed rail, Al Boraq. However, the uptake of green bonds markets remains limited in many Global South countries, despite strong potential to support large-scale, climate-aligned rail investments.

- Climate funds: Multilateral and bilateral climate funds are rapidly gaining importance. While still developing, they play a growing role in de-risking projects and improving bankability through concessional and viability gap funding, as well as crowding in private capital, particularly in emerging and developing economies.

- Carbon credit trading: Although their application in the transport sector has been mostly focused on the energy or biofuel markets and the EV car, these instruments hold significant potential for the railway transport sector, with emerging applications in Asia. With the proper certification mechanisms, these tradable emissions certificates could create new revenue streams for low-carbon rail projects, especially as carbon markets mature and expand.

Together, these nascent financing instruments represent a major opportunity to accelerate the development of rail based hinterland corridors. By lowering the cost of capital, reducing risk, and unlocking new revenue sources, they can help bring to market the large-scale investments required to decarbonize inland transport and strengthen port connectivity.

Thus, pursuing green-financed rail projects can not only be environmentally necessary but strategically advantageous, as it allows governments and ports to modernize their logistics systems, improve hinterland competitiveness against other gateway ports, and support long-term traffic growth, all while positioning national transport networks for a low-carbon future.

For ALG, accelerating the decarbonization of global supply chains requires a fundamental shift in hinterland transport. A modal shift towards rail offers the most effective pathway, but scaling rail based corridors demands robust institutional frameworks, technical and operational integration and, most importantly, credible investment structures capable of reducing risk and attracting long term capital to bridge the finance gap. In this context, we believe that the rise of green bonds, blended finance, and climate funds is creating an unprecedented opportunity to close this gap and accelerate implementation.

ALG brings more than 30 years of experience precisely in the areas that determine whether rail-based hinterland strategies can succeed in decarbonizing global supply chains: corridor planning, institutional design, and the structuring of financially viable investments. The firm has supported governments, port authorities and railway administrators in shaping rail initiatives that deliver lasting economic and environmental impact.

ALG has extensive experience supporting resource mobilization for rail based corridor initiatives, helping clients shape projects that can attract diversified, long-term capital sources. This includes advising on delivery models, preparing bankable investment cases, and supporting governments in accessing green financing mechanisms. ALG has helped clients articulate the emissions reductions, externality benefits, and climate alignment criteria needed for eligibility under these frameworks, as well as supported the mobilization of funds to feed these investments.

About the authors

Pol Blay I Sitges

MSc in Civil Engineering, specialized in logistics and multimodal transport. Consultant at ALG.

Joan Miquel Vilardell

PhD and MSc in Civil Engineering, and holds an MBA. Partner at ALG. Global Logistics Lead & Head of Africa Business.

– A key to future competition in businesses that are heavily dependent on supply chains")

")