Africa's ports are entering a new phase of development. For many years, most port investments were funded and managed by governments through state-owned port authorities. Today, that approach is increasingly giving way to concessions, PPPs, and long-term partnerships with private operators.

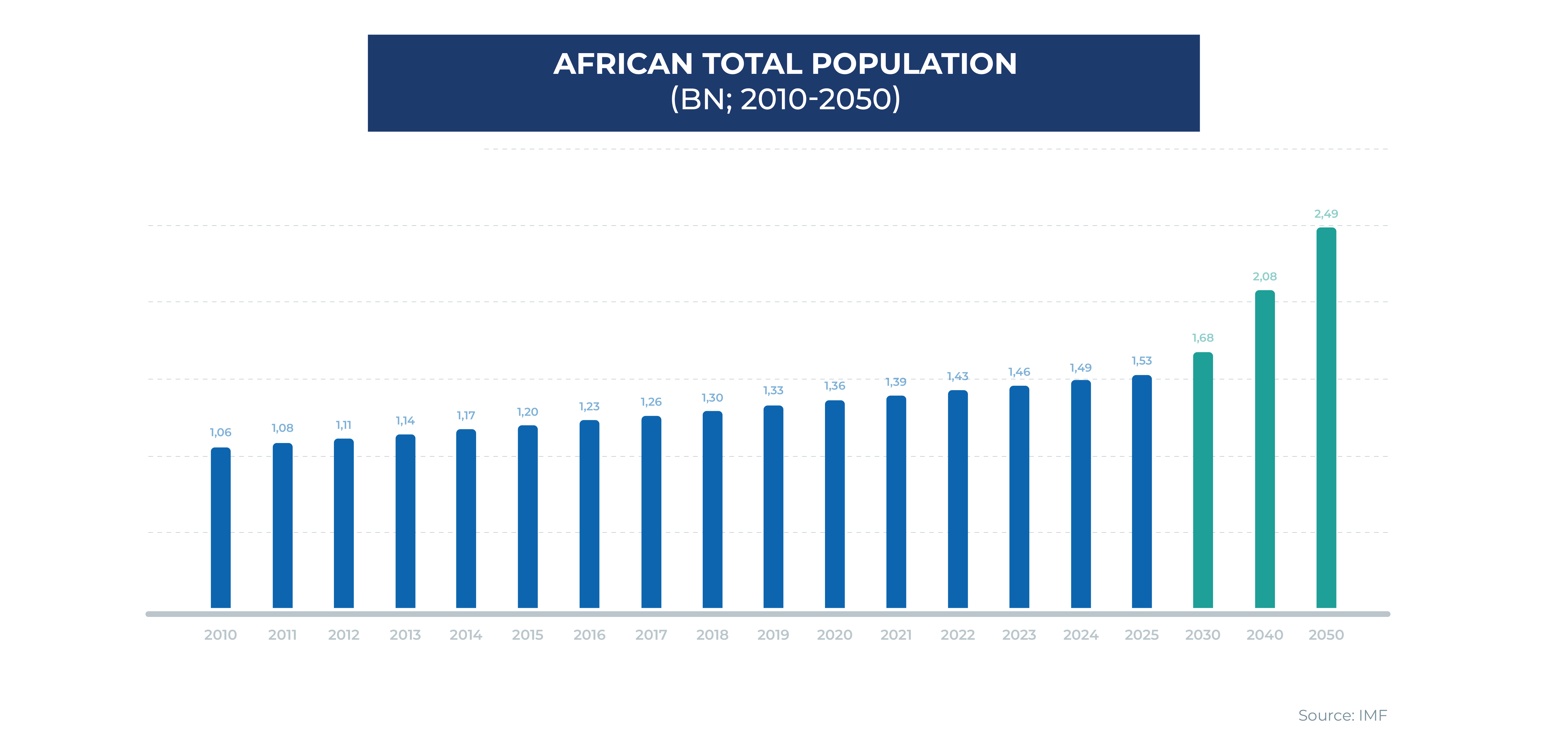

The reason is simple: demand is growing faster than existing infrastructure can keep up. Population growth, urbanization, industrialization, and regional trade are increasing pressure on ports across the continent. At the same time, many gateways continue to face congestion, capacity constraints, and weak inland connections that raise logistics costs and affect supply chain performance.

There is also a financial reality driving this shift. The African Development Bank estimates the continent's infrastructure needs at USD 130–170 billion per year, leaving an annual financing gap of USD 68–108 billion. In this context, PPPs are becoming less of an option and more of a necessity, helping governments mobilize capital, accelerate project delivery, and bring operational expertise into the sector.

For investors and terminal operators, this is opening up a broader range of opportunities. Increasingly, port projects are not just about adding capacity. They are also about improving trade corridors, strengthening logistics networks, and supporting wider economic development.

Why the transformation is accelerating

The current acceleration is the result of five mutually reinforcing forces: demand growth, infrastructure gaps, fiscal pressure, foreign capital competition, and the need to connect ports more effectively with inland markets.

Demand growth is increasing pressure on gateway ports

African ports are facing growing pressure as population growth, urbanization, and rising incomes continue to drive trade volumes across the continent. Demand for imported consumer goods, vehicles, construction materials, and energy products is increasing rapidly, particularly in large gateway markets such as Nigeria, Egypt, Kenya, and Ghana.

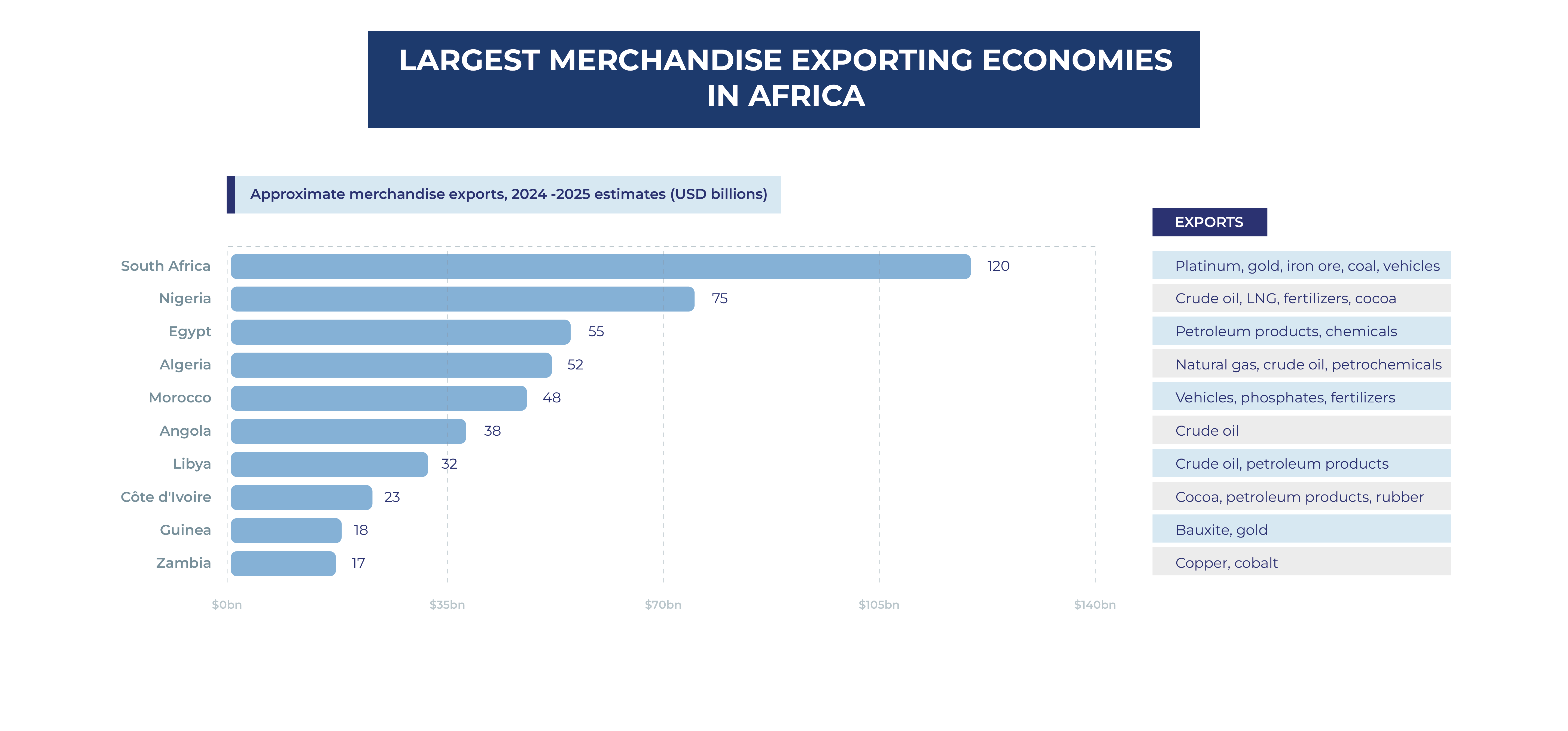

At the same time, expanding exports of minerals, agricultural products and energy commodities are generating additional demand for port capacity. Copper and cobalt exports from the Democratic Republic of Congo and Zambia, iron ore developments in Guinea, LNG projects in Mozambique and growing agricultural exports from West Africa are placing additional pressure on both bulk and container terminals. Major ports such as Lagos, Tema, Abidjan, Mombasa and Dar es Salaam must therefore accommodate rising cargo volumes while also serving as regional gateways for neighboring landlocked countries. In many cases, congestion, capacity constraints and weak inland links are becoming barriers to trade competitiveness, reinforcing the need for infrastructure expansion, operational modernization and greater private-sector participation.

Major ports such as Lagos, Tema, Abidjan, Mombasa and Dar es Salaam must therefore accommodate rising cargo volumes while also serving as regional gateways for neighboring landlocked countries. In many cases, congestion, capacity constraints and weak inland links are becoming barriers to trade competitiveness, reinforcing the need for infrastructure expansion, operational modernization and greater private-sector participation.

The infrastructure gap is too large for public budgets alone

Many African governments face fiscal constraints that limit their ability to finance large-scale port and transport infrastructure independently. While public investment remains important, budgetary pressures and competing development priorities are increasing the need for alternative financing mechanisms.

As a result, PPPs and concession models are becoming a central feature of port development across the continent. These structures allow governments to mobilize private capital, access operational expertise and accelerate project delivery while maintaining strategic oversight of critical infrastructure.

Recent projects illustrate this trend, suggesting that PPPs are no longer the exception in African ports. They are increasingly becoming the preferred model for delivering the next generation of maritime infrastructure.

Congestion and inefficiency are becoming trade competitiveness issues

Many African ports continue to face congestion, long dwell times, equipment shortages and weak hinterland connections. While the challenges vary by market, the result is translated into higher logistics costs, lower supply chain reliability, and reduced trade competitiveness.

The impact extends well beyond the port gate. As trade volumes grow, inefficient gateways can become bottlenecks for entire trade corridors, affecting exporters, importers, and inland economies that depend on them.

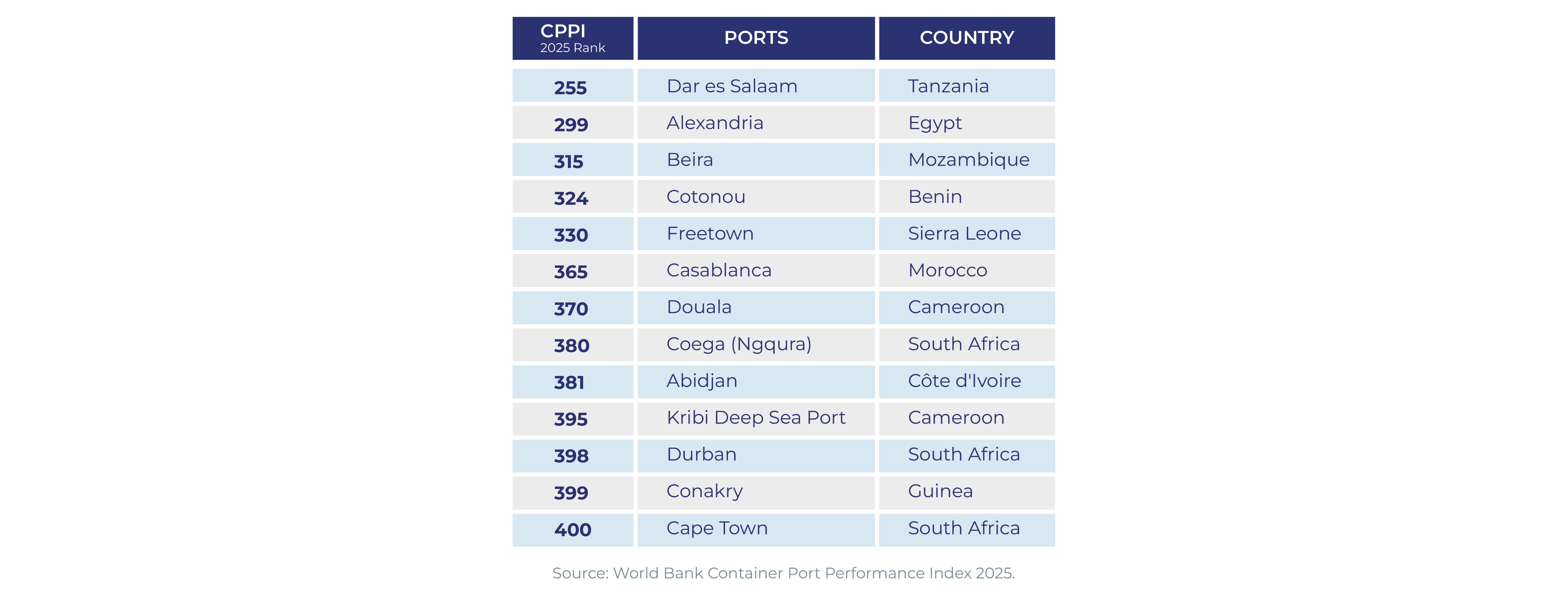

This is reflected in global port performance rankings, where many African ports continue to lag international benchmarks for efficiency and vessel turnaround times. As a result, PPPs are increasingly being used not only to finance infrastructure, but also to improve operational performance, introduce international best practices and accelerate modernization.  The performance gap between leading ports such as Djibouti and lower-ranked gateways such as Durban, Cape Town, Abidjan and Douala highlights the growing importance of operational efficiency, governance and private-sector participation

The performance gap between leading ports such as Djibouti and lower-ranked gateways such as Durban, Cape Town, Abidjan and Douala highlights the growing importance of operational efficiency, governance and private-sector participation

Global operators are competing for long-term exposure to African trade growth

Africa has become a strategic market for global port and logistics operators seeking long term exposure to trade growth. Unlike more mature regions, the continent continues to offer a combination of new concessions, greenfield developments and gateway assets with significant expansion potential.

The competitive landscape is increasingly shaped by a handful of operators building regional portfolios across the continent.

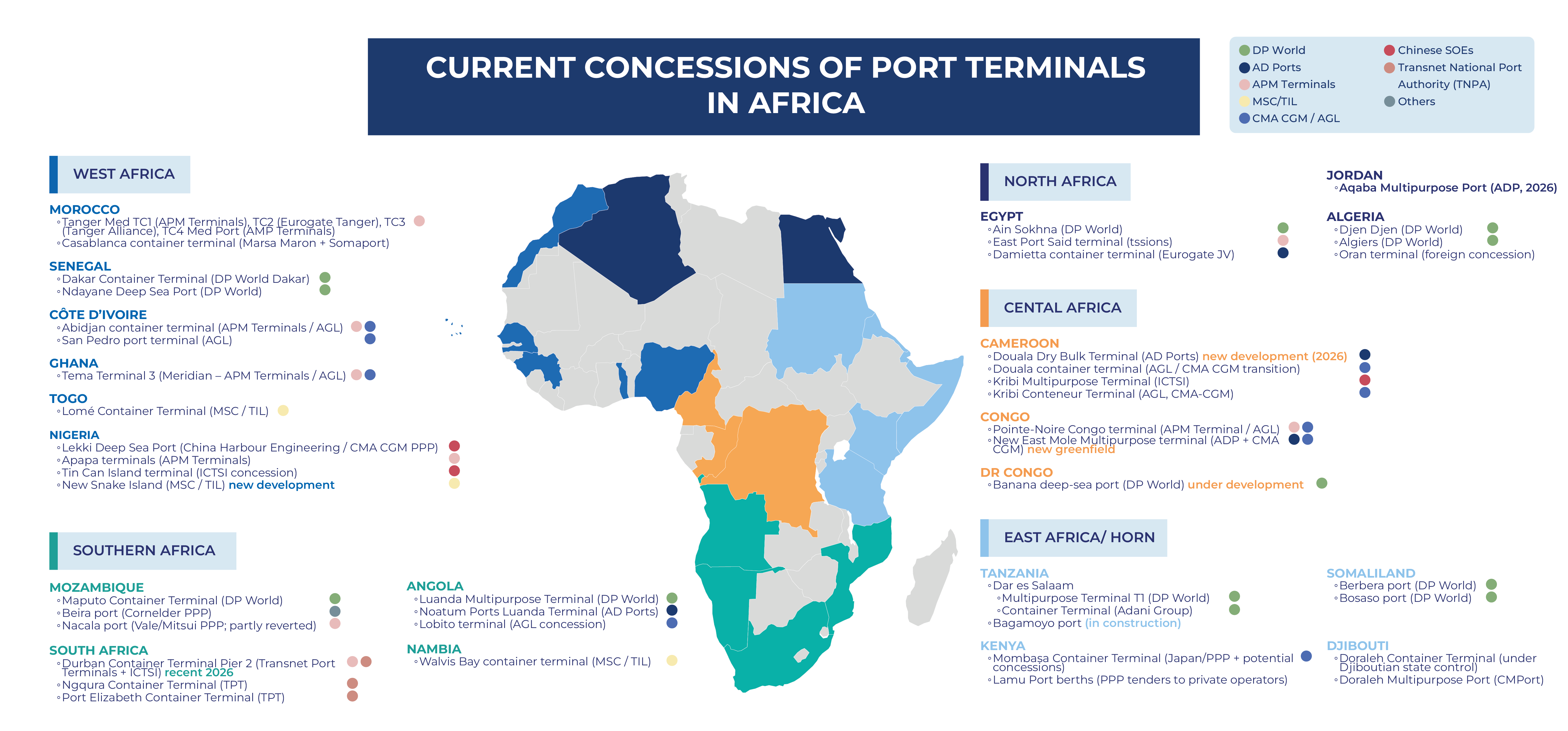

DP World now has operations or investments in more than ten African countries, while AD Ports Group has expanded rapidly through a series of acquisitions and concessions since 2022. APM Terminals, MSC/TiL and CMA CGM/AGL continue to strengthen their positions in key gateway and corridor markets.

This growing presence reflects a broader strategic objective: securing positions in the gateways that are expected to handle a rising share of Africa's future trade.

Port projects are increasingly corridor projects

Africa's most ambitious port developments are no longer standalone assets. They are increasingly being designed as part of broader trade, industrial and export corridors.

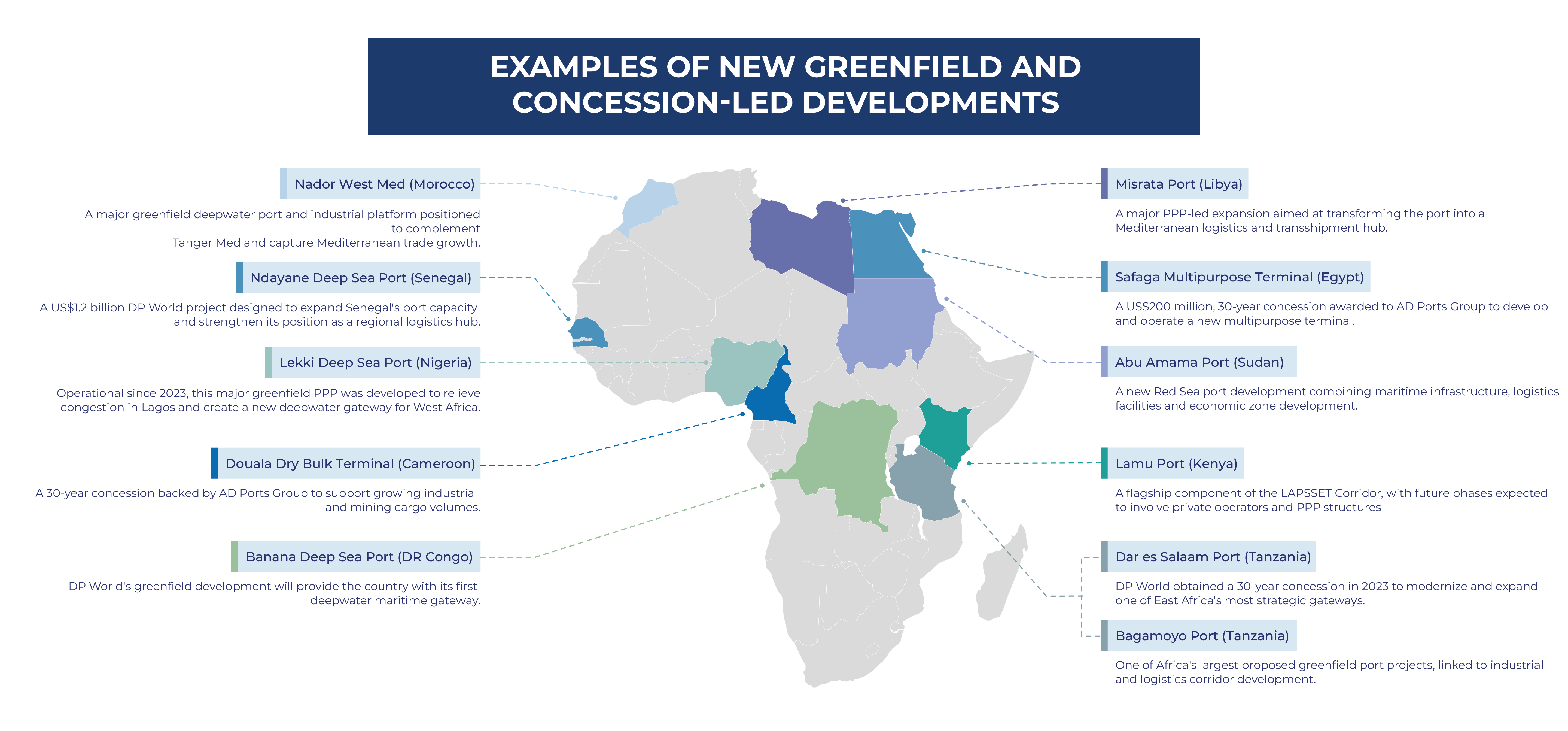

The Lobito Corridor is a clear example. Investments in Angola's Lobito Port are being complemented by rail links to the copper and cobalt regions of the Democratic Republic of Congo and Zambia, creating an alternative export route for critical minerals. Similarly, the LAPSSET Corridor aims to connect Kenya with Ethiopia and South Sudan through integrated port, road, rail and logistics infrastructure.

In North Africa, Tanger Med has developed alongside industrial and manufacturing clusters serving European markets, while Egypt's Suez Canal Economic Zone combines port infrastructure with logistics, industrial and export-oriented developments

These examples demonstrate that port investment decisions are increasingly linked to trade, industrial and export development strategies.

A market still dominated by greenfield developments

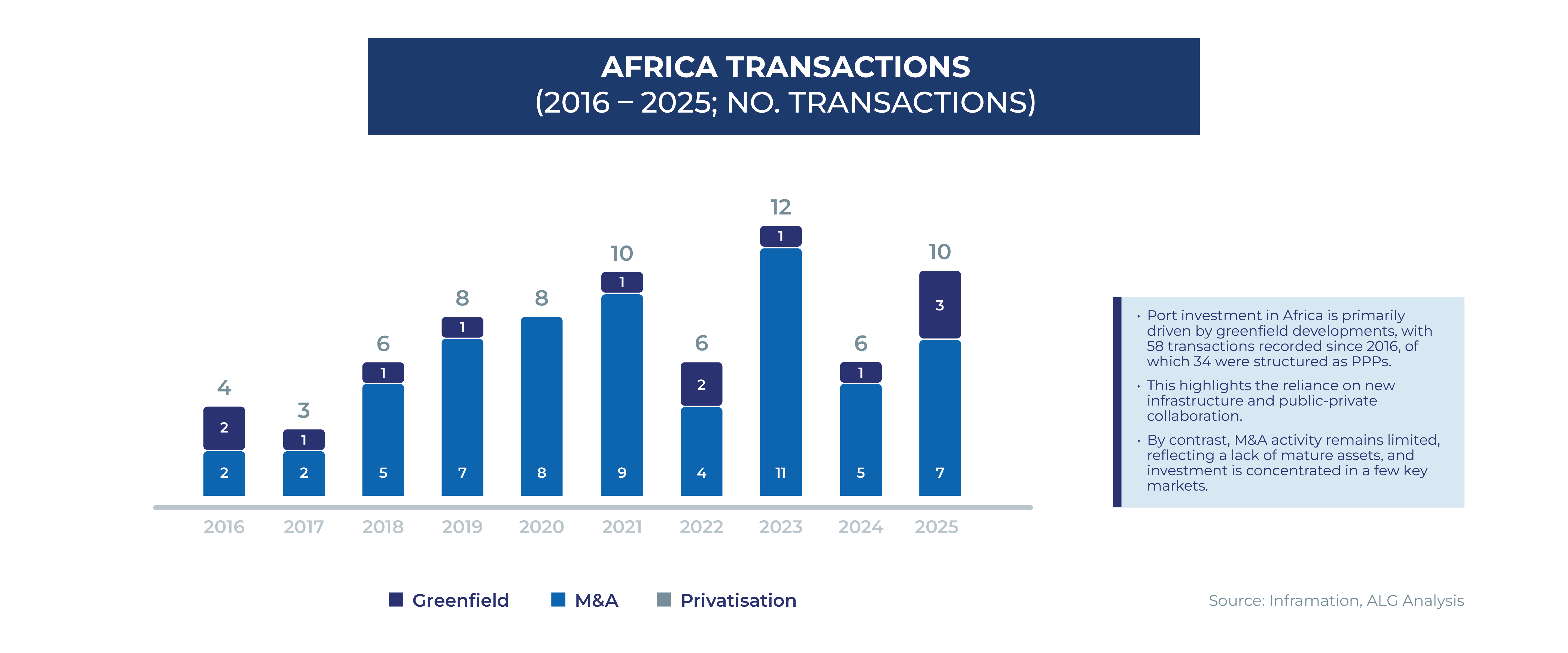

Unlike mature port markets, where transaction activity is largely driven by M&A, stake sales, concession renewals and portfolio optimization, Africa remains a development-led market. The transaction dataset records 73 port transactions between 2016 and 2025, of which 58 were greenfield developments, 14 were M&A transactions and only one was classified as privatization. In other words, around four out of every five recorded transactions were linked to the creation of new port infrastructure rather than the transfer of existing assets.

According to the transaction dataset, approximately 34 of the recorded greenfield transactions were structured as PPPs, illustrating the central role that concession models play in financing and delivering new port infrastructure across the continent.

According to the transaction dataset, approximately 34 of the recorded greenfield transactions were structured as PPPs, illustrating the central role that concession models play in financing and delivering new port infrastructure across the continent.

This highlights a distinctive feature of the African market: private investors are often participating at the asset creation stage rather than acquiring mature operating assets. As a result, transaction activity is heavily concentrated in project development, concession structuring and capacity expansion rather than secondary-market asset rotation.

Nearly 80% of recorded African port transactions since 2016 have involved new asset creation rather than asset transfers.

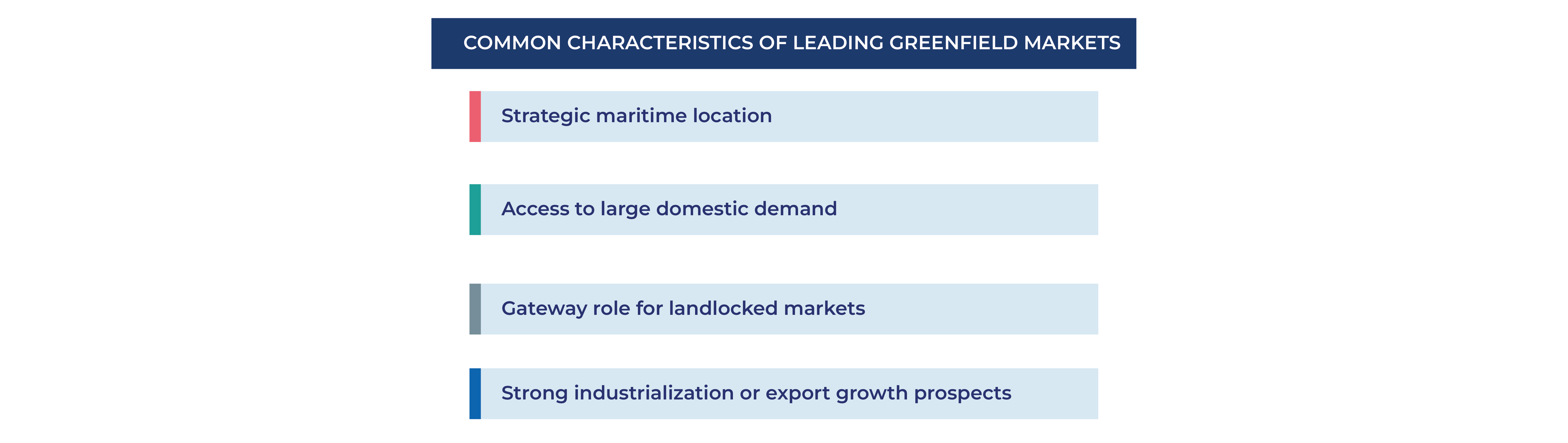

Which African countries lead greenfield activity and why?

Greenfield investment is concentrated in a relatively small group of markets that combine strategic location, strong trade flows, access to inland markets or industrial growth ambitions.

Egypt leads the continent, driven by the Suez Canal, an active concession program and the development of logistics and industrial zones. Nigeria continues to attract investment as it expands capacity to meet growing demand, while Tanzania is strengthening its position as a gateway to East and Central Africa.

Morocco has followed a different path, using ports such as Tanger Med to support industrialization, exports and nearshoring opportunities linked to Europe. Meanwhile, Ghana, Côte d'Ivoire and emerging markets such as the Democratic Republic of Congo and Senegal continue to attract investment through gateway and corridor-based projects.

Together, these markets show that port investment in Africa is increasingly driven by trade, industrial development and regional integration, rather than capacity expansion alone.

Different players are bringing different capabilities to the market

Africa's port sector is attracting a diverse group of investors and operators, each bringing different capabilities, investment approaches and sources of value creation. While these players often compete for the same opportunities, their contribution to port development extends beyond the provision of capital alone.

Integrated trade and logistics operators

Several global operators have expanded their presence in Africa through investments that combine ports with logistics, industrial and transport infrastructure.

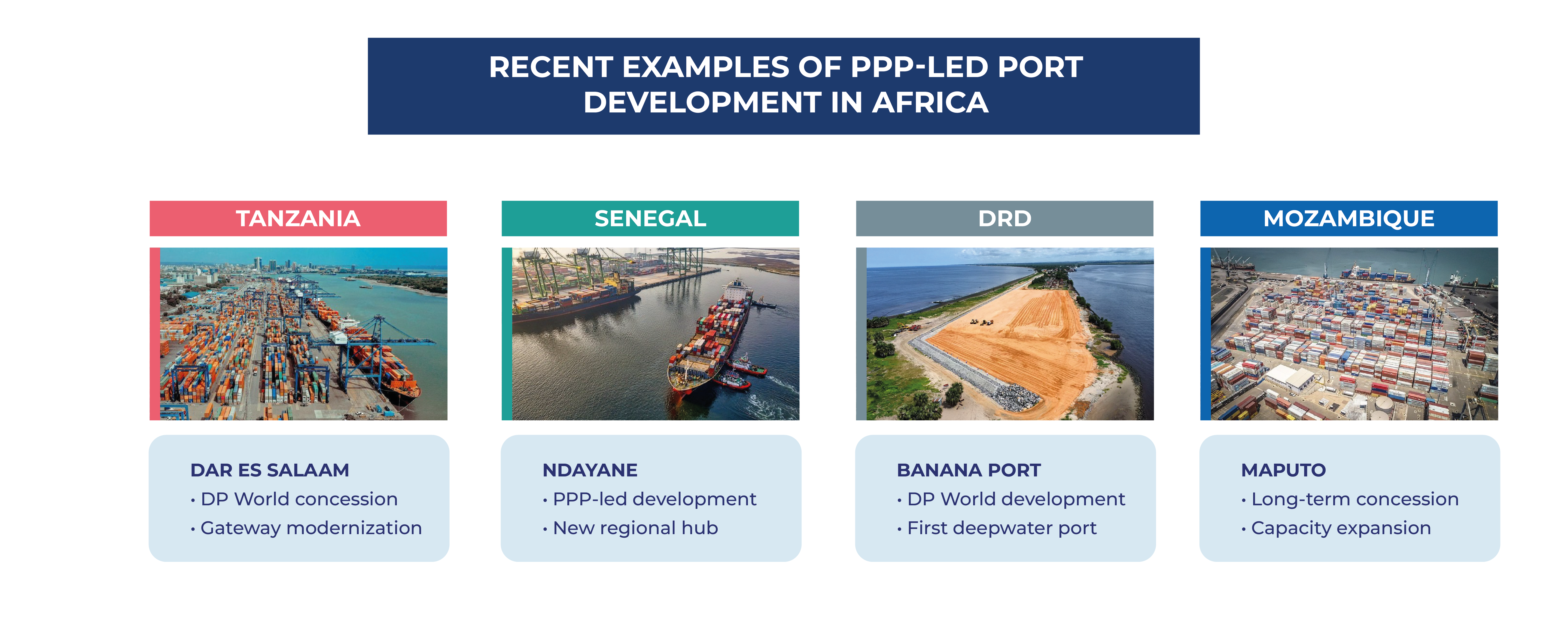

Recent projects involving DP World illustrate this broader approach. In Tanzania, the company secured the concession to operate and modernize Dar es Salaam Port, strengthening its role as a gateway for both Tanzania and several landlocked countries in East and Central Africa. DP World is also developing Ndayane Deep Sea Port in Senegal and Banana Port in the Democratic Republic of Congo, supporting the expansion of regional trade capacity and connectivity.

AD Ports Group has followed a similar strategy in Egypt, securing concessions in Safaga, Ain Sokhna and other Red Sea assets while investing in logistics and transport infrastructure linked to industrial and mining regions.

Together, these projects show how leading operators are investing not only in terminals, but also in the wider logistics, industrial and transport networks that support trade growth.

Shipping lines & linked operators

APM Terminals, MSC/TIL and CMA CGM/AGL represent another important group of investors in Africa's port sector. Their links to global shipping networks provide cargo volumes, operational expertise and access to international customers.

Across the continent, these operators have expanded through investments in strategic gateway terminals, including APM Terminals in Morocco, Côte d'Ivoire and Nigeria, MSC/TIL in West and Southern Africa, and CMA CGM through AGL and terminal investments across several markets.

Beyond capital, they bring direct connections to global trade routes, helping strengthen connectivity and improve service reliability.

Engineering, construction and infrastructure delivery specialists

Chinese companies have played a major role in the development of African port infrastructure, particularly in large-scale greenfield projects. China Harbour Engineering Company (CHEC), for example, participated in the development of Nigeria's Lekki Deep Sea Port, while Chinese firms have also been involved in projects such as Kribi in Cameroon, Doraleh in Djibouti and several ports along the East African coast.

Their key strength lies in delivering complex infrastructure projects, combining engineering expertise, execution capabilities and, in many cases, access to financing.

Infrastructure investors and financial capital providers

Infrastructure investors and development finance institutions are playing an increasingly important role in African port development. The Lobito Corridor, supported by the DFC, the European Union and the African Development Bank, highlights growing international interest in transport infrastructure linked to trade and critical mineral supply chains.

These institutions have also supported projects such as Lekki Deep Sea Port and Nador West Med, helping mobilize long-term capital for strategic infrastructure. As African port markets mature, their role in financing new developments and expansions is expected to grow.

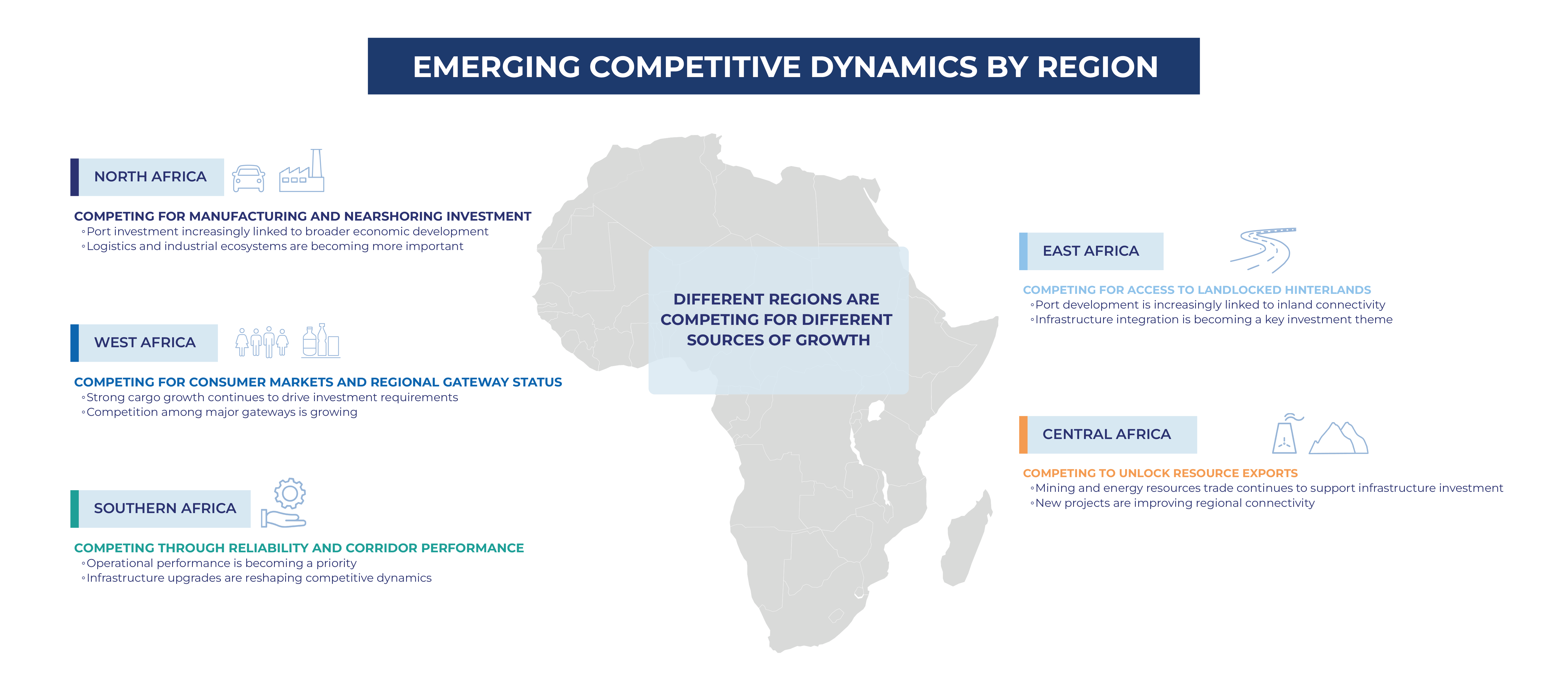

Where the next investment hotspots are emerging

Africa should not be viewed as a single port market. Different regions are attracting investment for different reasons, shaped by trade patterns, industrial development, export sectors and access to inland markets. As a result, the drivers of competition vary significantly across the continent.

North Africa is increasingly competing for manufacturing and nearshoring investment linked to Europe. In West Africa, competition is centered on gateway ports serving large consumer markets and regional hinterlands. East Africa is focused on improving access to landlocked markets through stronger trade corridors, while Central Africa's growth story is closely linked to mining and resource exports. In Southern Africa, the emphasis is increasingly on improving operational performance, reliability, and corridor efficiency. Together, these trends suggest that future investment opportunities will be shaped not only by port demand, but also by the ability of gateways to support broader industrial, logistics, and trade development objectives.

Together, these trends suggest that future investment opportunities will be shaped not only by port demand, but also by the ability of gateways to support broader industrial, logistics, and trade development objectives.

What could the next decade look like?

Africa's port sector is entering a new phase of competition. While terminal ownership remains important, future competitive advantage will increasingly depend on the ability to connect ports with logistics networks, industrial development and inland markets.

The next generation of projects is likely to extend beyond traditional terminal concessions, with greater emphasis on trade corridors, logistics platforms and integrated transport infrastructure. As a result, operators, investors and governments are increasingly evaluating ports as part of wider economic ecosystems rather than standalone assets.

Competition is also becoming more regional. Some markets are positioning themselves as manufacturing and export hubs, others as gateways to large consumer markets or strategic resource corridors. The ability to integrate these assets into efficient trade networks will be a key differentiator.

For governments, the challenge will be to attract investment while maximizing economic impact. For investors and operators, the opportunity lies in identifying the gateways, corridors, and partnerships best positioned to capture long-term growth.

The African port sector is therefore not only expanding, but it is also evolving. The projects most likely to succeed will be those that combine infrastructure, connectivity, and economic development into a compelling trade and logistics proposition.

At ALG, we have supported governments, port authorities, terminal operators, investors, development finance institutions, and logistics companies across Africa for more than two decades. This experience provides a unique perspective on the opportunities and challenges shaping the continent's evolving port sector, from PPP structuring and concession strategies to corridor development, logistics planning, and investment advisory.

About the authors

Anna Díaz Llop

Msc in Civil Engineering (with specialization in port planning). Senior Engagement Manager at ALG.

Joan Miquel Vilardell

PhD and MSc in Civil Engineering, and holds an MBA. Global Logistics Lead & Head of Africa Business. Partner at ALG.

")