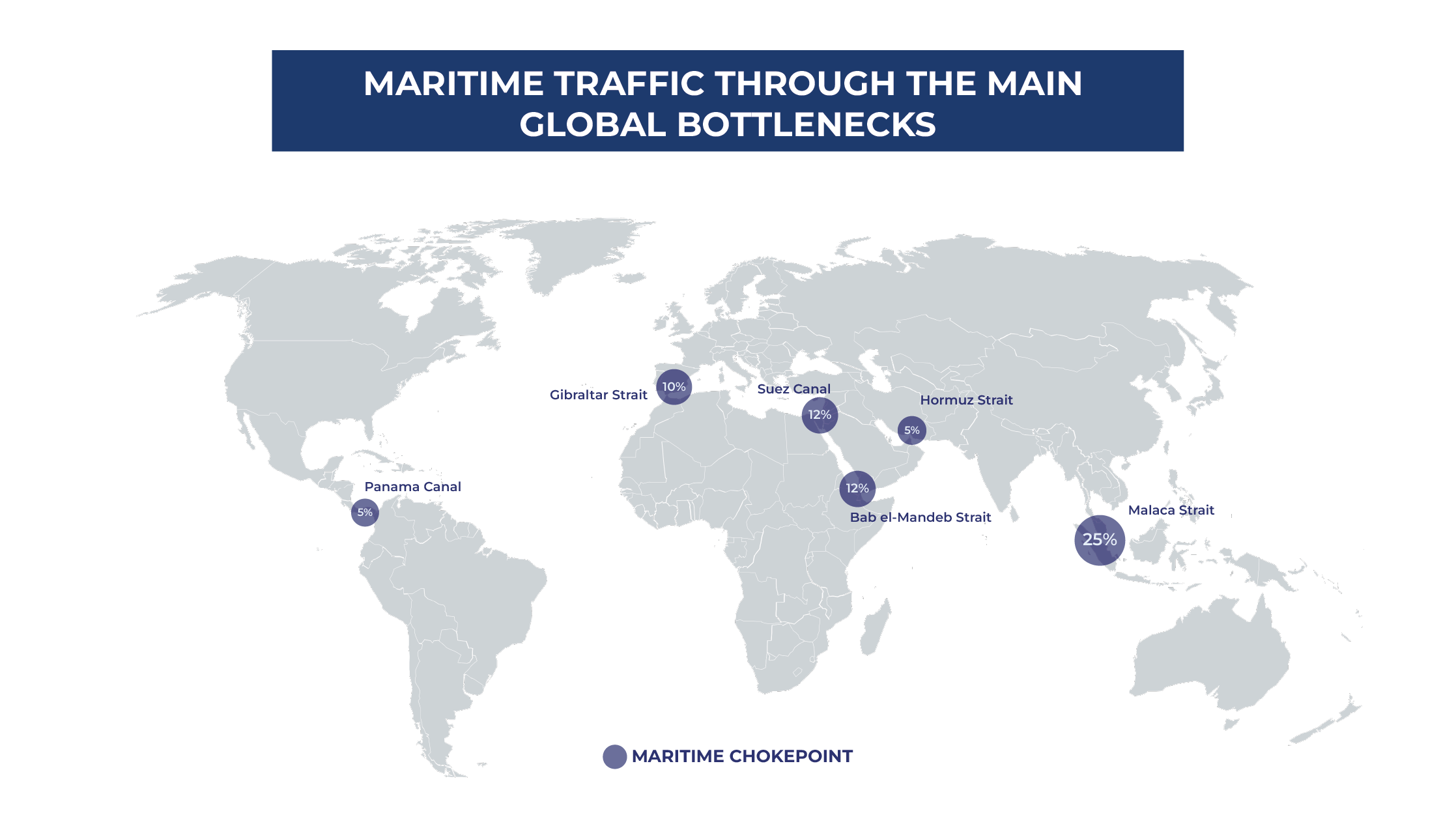

More than 80% of global trade travels by sea. Yet the system hinges on a handful of narrow maritime chokepoints and when one fails, the shock is immediate and global.

Recent events have shown how fragile this dependency can be. For example, in 2021 the blockage of the Suez Canal by the Ever Given brought one of the world’s most critical trade arteries to a standstill, triggering delays that rippled across continents. More recently, drought conditions linked to El Niño have constrained capacity at the Panama Canal, pushing transit times into double digits and disrupting global shipping schedules.

At the same time, security threats have added a new layer of risk. Attacks by the Houthi movement on commercial vessels in the Red Sea have forced shipping companies to reroute traffic around the Cape of Good Hope, significantly increasing transit times and costs. The episode highlights how even relatively localized conflicts can disrupt critical maritime corridors with global consequences.

Now, attention has shifted to the Strait of Hormuz. Rising geopolitical tensions involving Iran are placing pressure on one of the most strategically sensitive routes in the world, exposing once again a structural weakness at the heart of global trade.

These chokepoints, though often overlooked, are essential to the functioning of the global economy. They enable the continuous flow of energy, raw materials, and goods, acting as critical junctions in highly optimized supply chains. When access is restricted, the consequences are immediate: delays cascade, logistics costs rise, and market volatility intensifies.

What this reveals is not just the importance of these routes, but the risks embedded in such a concentrated system. Global trade has been built for efficiency, minimizing costs and transit times, but far less attention has been given to resilience. As disruptions become more frequent, this trade-off is becoming increasingly visible.

The situation in the Strait of Hormuz brings this tension into sharp focus. Roughly 5% of global trade flows through this corridor, much of it energy exports. As pressure mounts, the effects are already materializing: constrained flows, strained regional logistics, and sharp reactions in global markets. In recent weeks, crude oil prices have surged by more than 60%, underscoring how quickly a localized disruption can escalate into a global economic shock.

In the end, the question is no longer whether these chokepoints matter, it is whether the global system can afford to remain so dependent on them.

Inside the Hormuz disruption: trade reconfigured in real time

Three weeks into the conflict with Iran, the Strait remains far from a secure corridor for commercial navigation, raising urgent questions about the viability of traditional shipping routes and accelerating the search for alternative gateways into and out of the Middle East.

Rather than waiting for conditions to stabilize, governments, energy producers, and shipping lines are actively redesigning supply chains. The objective is clear: reduce dependence on Hormuz while maintaining trade continuity under increasingly volatile conditions. What is emerging is not a temporary adjustment, but a structural shift in how trade flows across the region spanning transport modes, infrastructure use, and risk management strategies.

Exports: constrained alternatives to a critical corridor

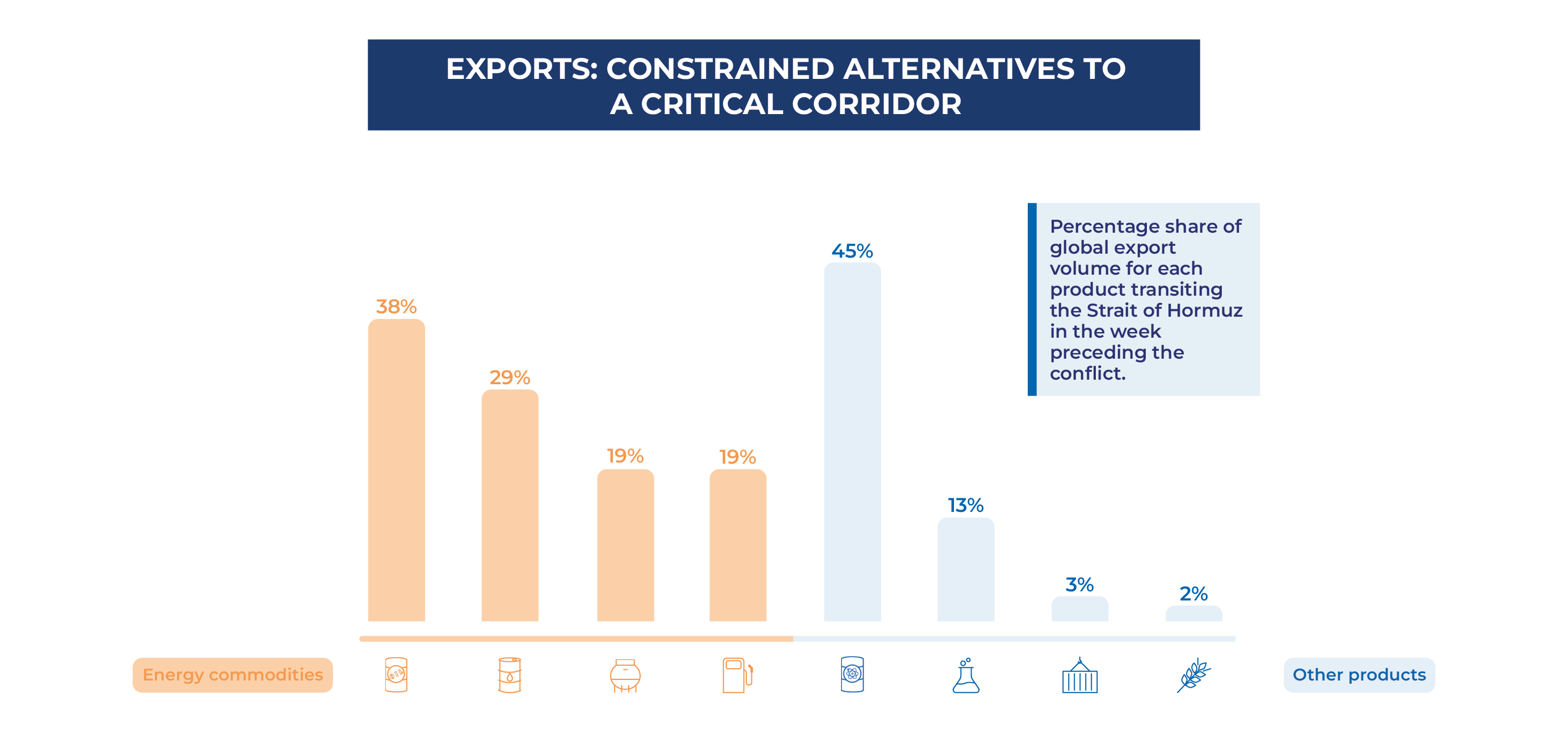

The Strait of Hormuz is one of the world’s most important energy gateways, handling a substantial share of global hydrocarbon exports alongside fertilizers, chemicals, and other industrial commodities. Under normal conditions, around 20 million barrels of crude oil per day (38% of global exports) transit through this narrow passage, illustrating the scale of global exposure concentrated in a single route.

The Strait of Hormuz is one of the world’s most important energy gateways, handling a substantial share of global hydrocarbon exports alongside fertilizers, chemicals, and other industrial commodities. Under normal conditions, around 20 million barrels of crude oil per day (38% of global exports) transit through this narrow passage, illustrating the scale of global exposure concentrated in a single route.

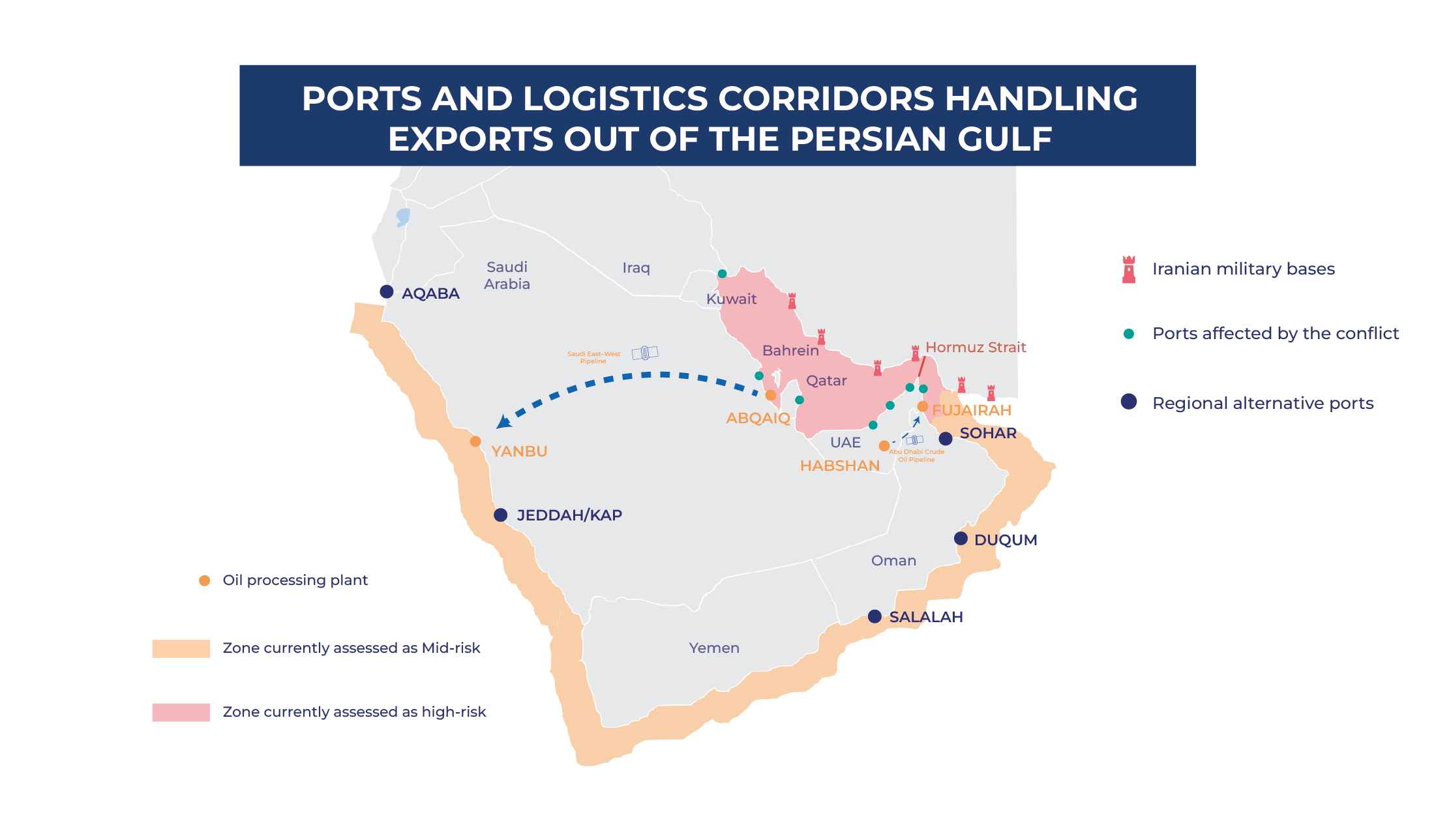

As tensions escalate, exporters are turning to overland alternatives. Pipeline networks—such as the Saudi East–West Pipeline (Petroline), the Abu Dhabi Crude Oil Pipeline (ADCOP), and the Iraq–Turkey corridor to the Mediterranean—offer partial relief. In theory, these systems provide up to 7 million barrels per day of bypass capacity. In practice, however, closer to 5 million barrels can be redirected to international markets, with the remainder tied to domestic or regional demand.

Even these alternatives face hard limits. Combined capacity from Petroline and ADCOP is estimated at around 4.7 million barrels per day, while actual flows through ADCOP are significantly lower due to terminal and operational constraints. Meanwhile, Iraq’s northern export routes remain underutilized, forcing authorities to rely on trucking volumes of up to 200,000 barrels per day—a costly and inefficient stopgap.

Storage and bunkering infrastructure have become critical buffers. The Port of Fujairah, in particular, has emerged as a key hub outside the Strait, with tens of millions of barrels in storage capacity and expanding underground reserves. However, its growing strategic importance has also made it a target. Recent missile strikes have partially disrupted operations, underscoring a central reality: even alternative nodes remain exposed to geopolitical risk.

Ultimately, these workarounds cannot replicate the scale, efficiency, or cost advantages of maritime flows through Hormuz. The conclusion is unavoidable: diversification of export routes and sustained investment in resilient infrastructure are no longer strategic options, but necessities.

Imports: rising costs and reconfigured supply chains

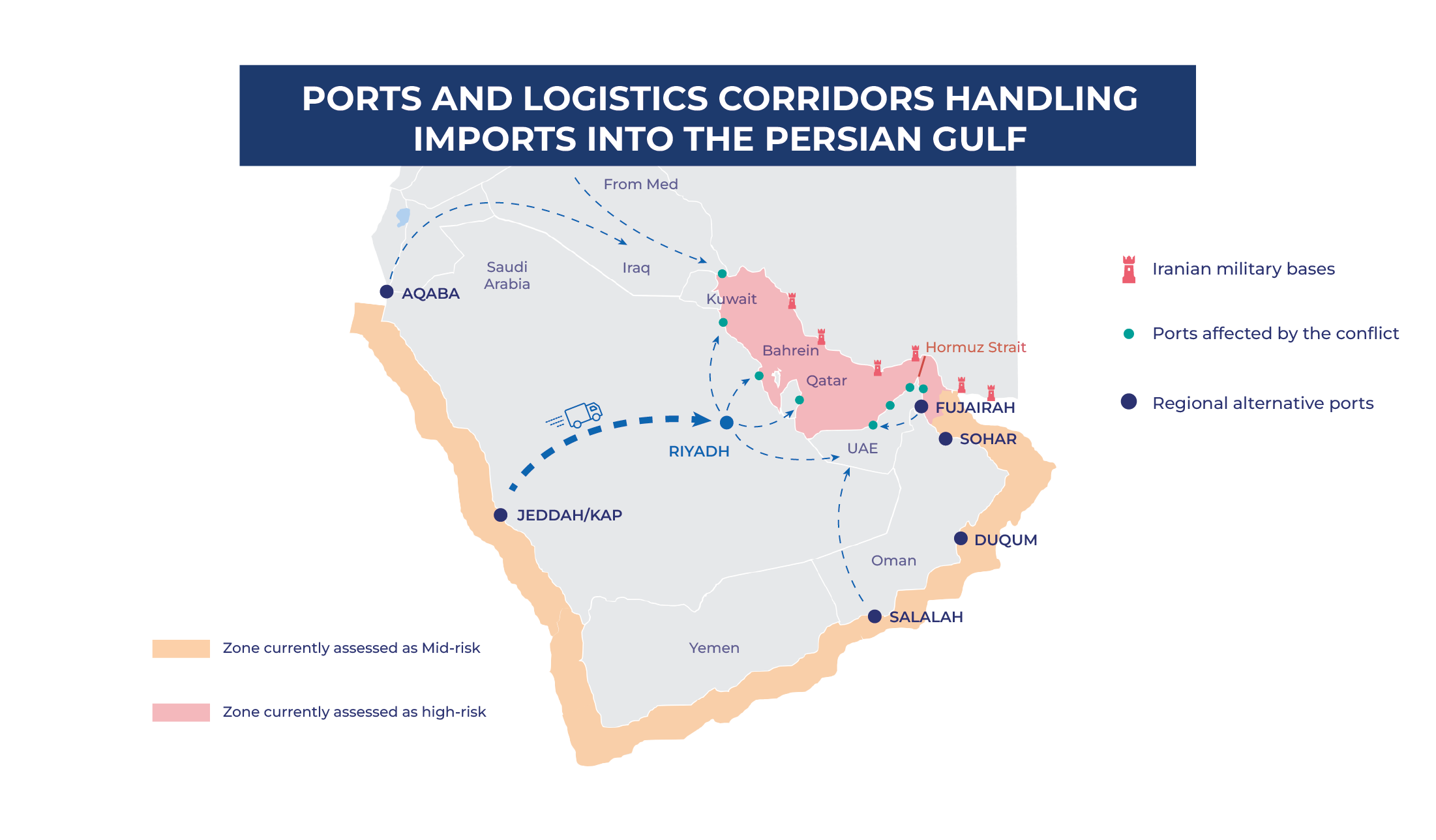

On the import side, the disruption is equally profound. The Gulf Cooperation Council (GCC) remains heavily dependent on external supplies, with food imports alone accounting for up to 85% of demand. This reliance extends to construction materials, industrial inputs, refined fuels, and consumer goods—making supply continuity a critical concern.

As vessel movements are delayed or rerouted, congestion is building at alternative entry points, logistics costs are rising sharply, and delivery times are becoming increasingly unpredictable. In response, cargo is being redirected toward less exposed ports along the Red Sea and Arabian Sea, including the ports of Jeddah and Aqaba. From there, goods are transported inland via road and rail, supported by an expanding network of dry ports and intermodal hubs. Also, ports in Oman like Salalah or the port of Fujairah are acting as alternative gateways, especially for the UAE.

As vessel movements are delayed or rerouted, congestion is building at alternative entry points, logistics costs are rising sharply, and delivery times are becoming increasingly unpredictable. In response, cargo is being redirected toward less exposed ports along the Red Sea and Arabian Sea, including the ports of Jeddah and Aqaba. From there, goods are transported inland via road and rail, supported by an expanding network of dry ports and intermodal hubs. Also, ports in Oman like Salalah or the port of Fujairah are acting as alternative gateways, especially for the UAE.

At the same time, maritime routes are being reconfigured. Where possible, shipping lines are bypassing the Strait altogether, opting for longer but more predictable routes. Transshipment strategies are also shifting toward out-of-strait hubs, which consolidate cargo before distributing it into the Gulf via feeder services.

The trade-off is clear: greater resilience comes at the cost of efficiency. Longer routes increase fuel consumption, while additional handling and inland transport drive up overall logistics costs. These pressures are already feeding into broader concerns around supply chain stability, food security, and regional price volatility.

A structural shift toward resilience

Taken together, these dynamics point to a deeper transformation. The region is moving away from a model built primarily on cost-efficient maritime flows toward one that prioritizes flexibility, redundancy, and inland connectivity.

The disruption of the Strait of Hormuz has made one thing clear: resilience is no longer a secondary consideration in trade design, it is becoming its defining principle.

From shock to strategy

Taken together, the disruptions across the Suez Canal, the Panama Canal, the Red Sea and most recently the Strait of Hormuz point to a persistent structural reality: global trade remains heavily dependent on a limited number of strategic maritime corridors. When instability affects any one of these nodes, the impact quickly extends beyond shipping lanes, disrupting logistics networks, freight markets, and industrial supply chains worldwide.

What these events make increasingly clear is that resilience is not defined by individual assets alone. Ports, canals, and shipping routes are only as effective as the systems that connect them. The real strength of global trade lies not in isolated infrastructure, but in the corridors that integrate them into coherent, flexible networks.

In this context, intermodal connectivity and “landbridges” are emerging as a central pillar of resilience. Corridors that link maritime gateways with rail, road, and inland logistics platforms provide the flexibility needed to reroute flows and maintain continuity when pressure builds around a specific chokepoint.

These systems do not eliminate volatility, but they change how it is managed. Diversified corridors and multiple routing options allow supply chains to absorb shocks, reduce systemic exposure, and introduce the redundancy that an increasingly uncertain trade environment demands.

Building this resilience, however, comes at a cost. Developing integrated logistics corridors requires investments of a scale and complexity that rarely fall within the reach of a single actor. Their success depends on coordinated planning between governments, infrastructure operators, and private investors. Public–private partnerships are therefore becoming a critical mechanism to mobilize capital, align incentives, and accelerate delivery.

What is emerging is a shift in mindset. The objective is no longer simply to optimize for cost and efficiency, but to design systems that can withstand disruption. Expanding intermodal alternatives, diversifying trade corridors, and strengthening coordination across stakeholders will be essential to reducing exposure to a handful of critical routes.

The question is no longer whether disruptions will occur, but how prepared supply chains are to absorb them. Which corridors will emerge as the next strategic alternatives? How far are governments and industry willing to go to build true redundancy into the system? And ultimately, will the next phase of global trade be defined by efficiency alone, or by resilience?

About the authors

Ignacio Rodríguez de la Rúa

MSc and BSc in Civil Engineering. His areas of expertise include PPP structuring, the definition of strategic and commercial guidelines, business development, M&A advisory and others worldwide, all within the maritime sector. Senior Engagement Manager at ALG.

Javier Ramos

MSc and BSc in Maritime Engineering, specialized in vessel dynamics and ship systems. Experience in global market analysis and commercial strategy within the maritime sector for numerous commodities. Consultant at ALG.

Fernando Díaz

BSc in Civil Engineering and Business Administration and MSc in Civil Engineering. He focuses on maritime infrastructure transactions and advisory. Part of the Maritime team in ALG.

")