Why are technological giants such as Amazon investing hundreds of millions in satellite ground infrastructure?

Market trends increasingly show that value lies not in ownership, but in access. Music albums and movie DVDs, for example, have largely been replaced by streaming platforms like Spotify and Netflix.

The space industry is no exception. For decades, operating a satellite meant investing hundreds of millions of dollars in ground infrastructure — antenna arrays, uplink/downlink systems, operations centers. Now, through a new concept called Ground Infrastructure as a Service (GIaaS), companies can apply the same pay-per-use, on-demand principles to one of the most technically demanding sectors in the world: satellite ground operations.

Today, Amazon and other companies are turning physical ground infrastructure into a cloud-native, on-demand service, allowing private companies and governments to access global ground station capacity without owning a single antenna.

This concept is expected to evolve to a multi-billion-dollar industry in the next decade, attracting large technological corporations such Amazon, and also reshaping the strategies of traditional satellite operators such as Eutelsat, who recently planned a divestment of more than >500 M USD of ground infrastructure, a clear sign of how the as-a-service model will reshape the sector.

The current context

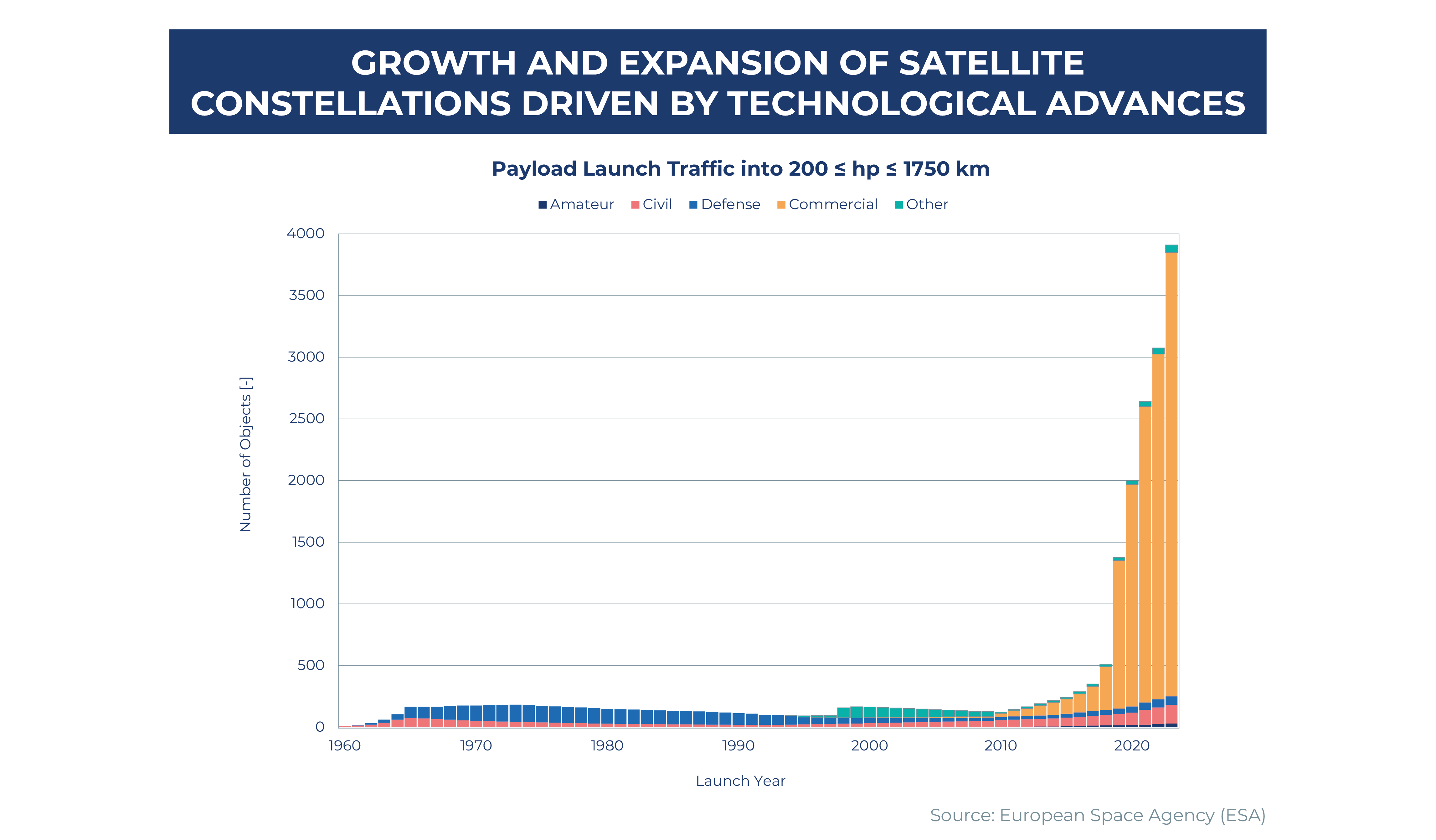

This “as-a-service” model makes even more sense in the current state of the space sector, which is undergoing a phase of rapid transformation, with lower entry barriers. What was once a domain limited to governments and large space agencies is now opening up to a wider range of players with more agile, commercially driven approaches, thanks to falling launch costs and miniaturized satellites.

This democratization of space has led to a significant increase in the number of satellite missions, particularly LEO (Low-Earth Orbit) missions, as well as a growing number of applications built on satellite data. From startups to large enterprises, more organizations are deploying or relying on space-based capabilities, which in turn increases the demand for ground infrastructure to control, monitor, and process mission data.

At the same time, operational requirements are becoming more demanding. Many modern satellites, particularly small satellites, have limited onboard storage capacity, which drives the need for frequent data downlinks and near real-time access to information. This increases the dependency on ground infrastructure and requires more frequent contact windows and higher availability of ground stations.

However, building and operating this infrastructure represents a significant cost, often reaching hundreds of millions of dollars at a global scale. For many missions, especially smaller ones, this level of investment is difficult to justify. Additionally, dedicated ground infrastructure is inherently underutilized, as satellites only connect during specific time windows, leaving assets unused for large portions of time.

In this context, shared infrastructure models become not only attractive but necessary. By enabling multiple missions to use the same ground resources, GIaaS improves utilization, reduces costs, and provides flexible, on-demand access to critical capabilities – positioning itself as a key enabler of the new space economy.

Understanding GIaaS

While satellites operate in orbit high above the Earth, their functionality depends critically on the ground segment. This terrestrial infrastructure serves as the interface between space-based assets and the organizations that rely on their services, enabling command, control, telemetry, and the delivery of mission data.

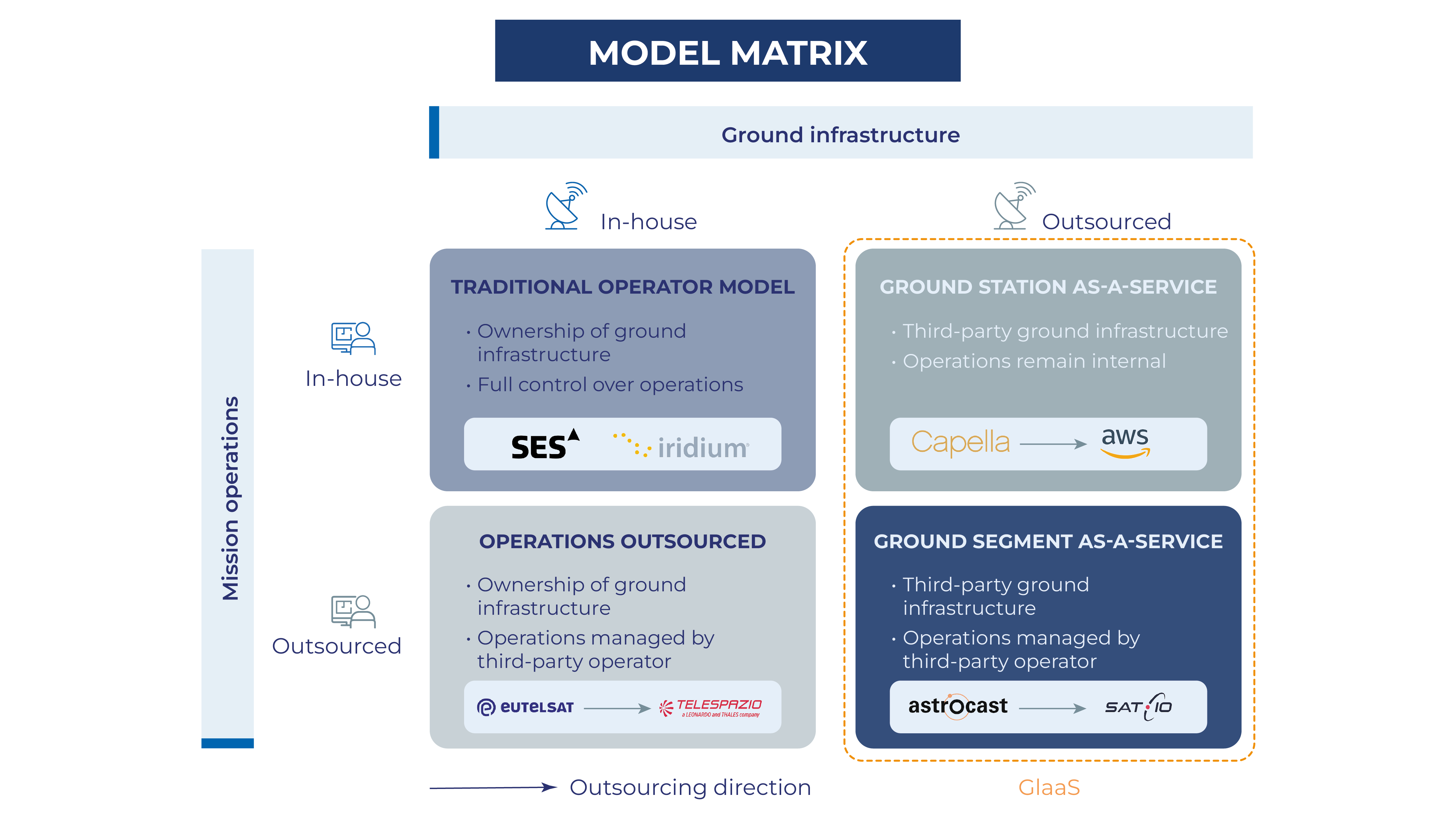

The ground segment can be managed in different ways. Operators may handle both the ground infrastructure and mission operations internally, retaining full control, or they may choose to outsource one or both functions to specialized providers. Ground infrastructure includes the physical stations, antennas, and network systems needed to communicate with satellites, while mission operations cover the planning, execution, and monitoring of satellite activities and data.

When ground infrastructure is outsourced, regardless of whether mission operations remain in-house or are also delegated, this model is referred to as GIaaS.

In practice, GIaaS usually provides operators with several key capabilities:

- Shared global ground antenna networks: Operators can tap into a distributed network of ground stations worldwide, giving them broad coverage and flexibility.

- Cloud-based satellite control and monitoring: Functions that used to require on-site hardware – like sending commands and checking the satellite’s status – can now be managed remotely in the cloud, providing flexibility and scalability.

- Managed mission operations: Operators can plan and schedule satellite passes, route data, and interact with mission systems remotely via web portals or APIs, all without the need for an on-site control center.

- Usage-based commercial models: Operators pay for what they use (e.g., per satellite pass, per minute of antenna time, or per gigabyte of data), turning capital expenses into operational costs.

These elements illustrate how GIaaS delivers cloud-like capabilities to satellite operations, offering versatile, easily scaled, and cost-efficient ground infrastructure.

Main benefits and risks

Taken together, these service models fundamentally change how satellite operators approach the ground segment. By moving away from owning infrastructure toward on-demand services, these models provide a range of practical operational benefits, which are summarized in the diagram below:

At the same time, adopting GIaaS introduces strategic and operational risks that operators must carefully manage. Dependence on third-party providers can limit flexibility in adjusting services or switching partners. Data sovereignty and security concerns are also critical, especially when mission data crosses national boundaries or relies on shared infrastructure. Additionally, regulatory constraints may impact how ground services are accessed and operated across different regions, potentially affecting mission planning and compliance. Balancing these risks with the operational benefits of GIaaS is essential to ensure that the service supports both short-term mission goals and long-term strategic objectives.

GIaaS market

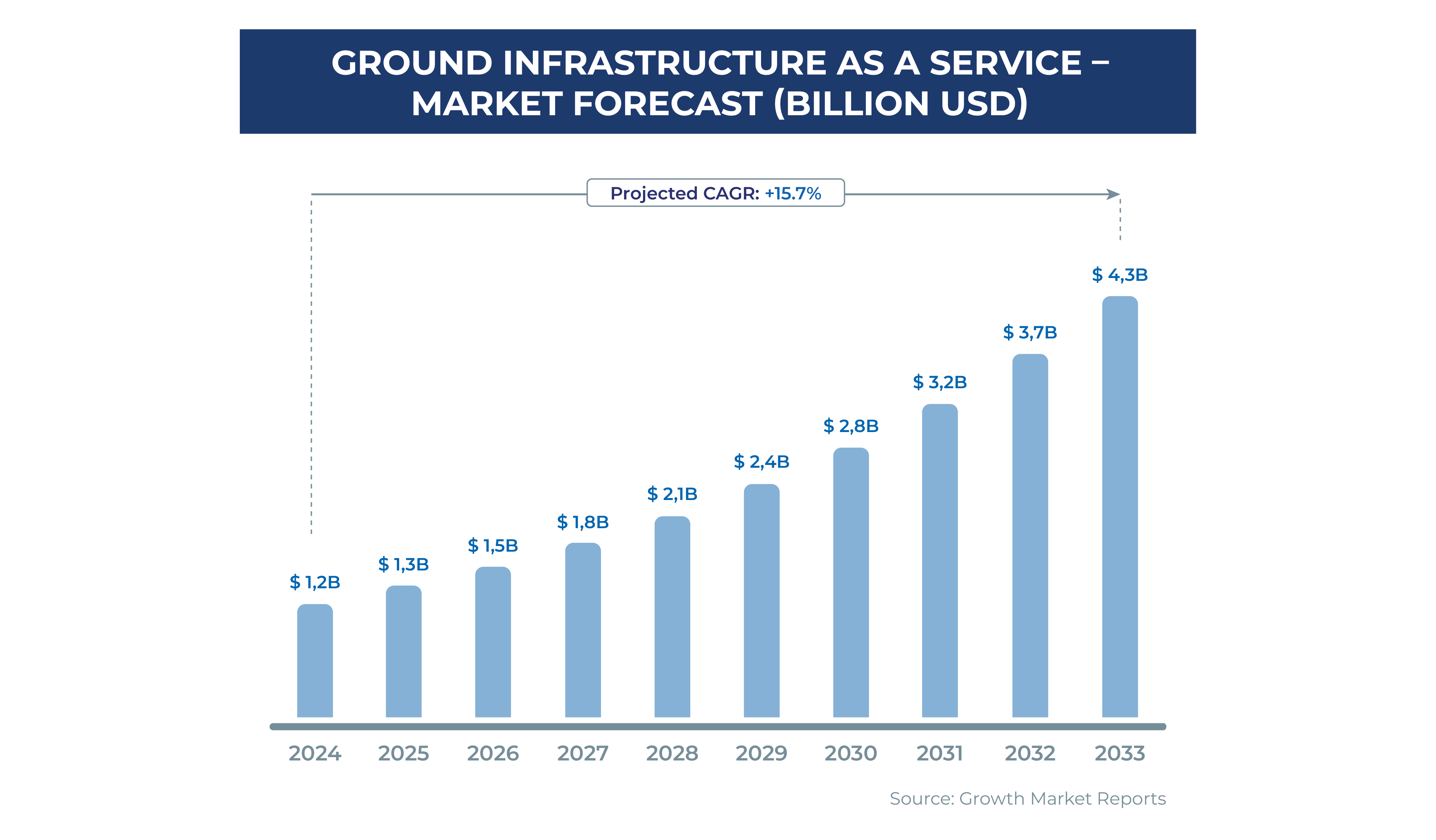

The global Ground Infrastructure as a Service market is estimated at around USD 1.16 billion in 2024. Fueled by the rapid expansion of small satellite constellations, growing demand for real-time data, and the shift from capital-intensive ground infrastructure to on-demand access, the market is projected to grow steadily over the next decade. By 2033, GIaaS could reach approximately USD 4.3 billion, reflecting strong double-digit annual growth. While specific definitions vary, the trend is unmistakable: service-based ground infrastructure is quickly becoming a central part of satellite operations rather than a niche solution.

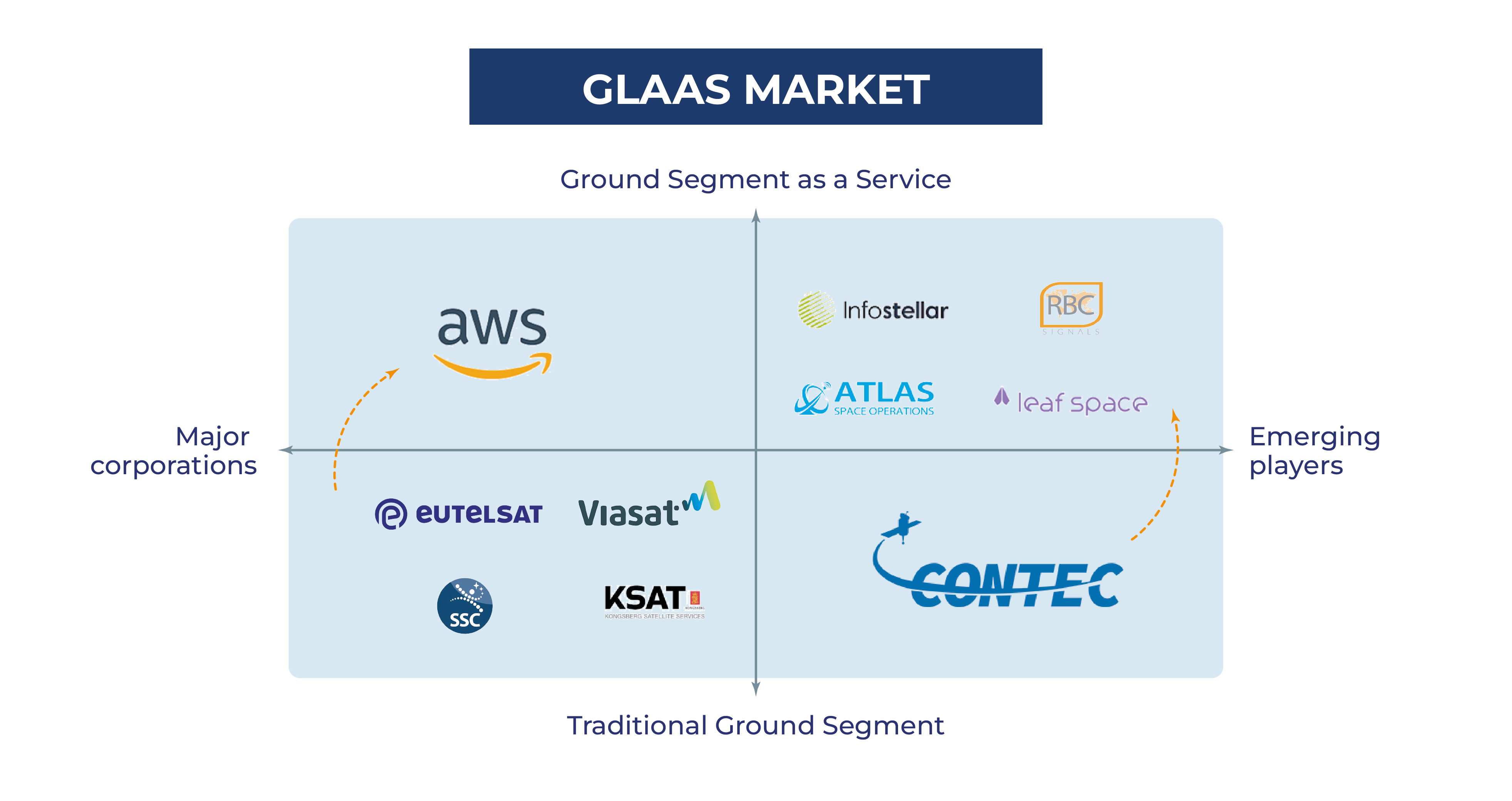

This strong growth trajectory is reshaping the competitive landscape. As ground capabilities transition from owned infrastructure to as-a-service models, a new generation of specialized providers has emerged, including Leaf Space, Infostellar, Atlas Space Operations, and RBC Signals. CONTEC, which began as a traditional ground segment operator, has rapidly adapted and transitioned to Ground Segment as a Service.

This strong growth trajectory is reshaping the competitive landscape. As ground capabilities transition from owned infrastructure to as-a-service models, a new generation of specialized providers has emerged, including Leaf Space, Infostellar, Atlas Space Operations, and RBC Signals. CONTEC, which began as a traditional ground segment operator, has rapidly adapted and transitioned to Ground Segment as a Service.

At the same time, large technology companies such as Amazon Web Services (AWS) are positioning themselves at the center of this transition, leveraging their global cloud infrastructure and integrating managed ground station networks directly into their cloud environments.

In contrast, established ground segment companies such as Viasat, KSAT (Kongsberg Satellite Services), and SSC Space continue to operate large, asset-intensive ground networks, primarily serving institutional and major commercial missions. While some are exploring incremental modernization, their models remain largely rooted in ownership and long-term infrastructure deployment rather than fully virtualized, on-demand service delivery.

A noteworthy case is that of Eutelsat, which in 2024 planned to sell a majority stake in part of its terrestrial ground infrastructure to a private equity partner. The move was intended to separate asset-heavy infrastructure from service-oriented operations and generate capital to support its broader satellite strategy. However, the French government ultimately blocked the transaction on national security grounds, preventing the sale. Even so, the case highlights the growing pressure on traditional operators to rethink ownership-heavy models and consider more flexible, scalable approaches like GIaaS.

Conclusions

In conclusion, Ground Infrastructure as a Service (GIaaS) is transforming the satellite industry by shifting the ground segment from an asset-heavy model to a flexible, on-demand service. This evolution lowers barriers to entry to new players, improves scalability, and accelerates time-to-market, while reshaping competition through the rise of specialized providers and the entry of major cloud players. However, it also introduces challenges around dependency, data governance, and regulation. Satellite operators who effectively balance these trade-offs and embrace service-based models will be better positioned to achieve efficiency, agility, and long-term competitiveness.

About the authors

Mario Cano

BSc in Aeronautical Engineering, MSc in Astronautics and Space Engineering, and MSc in Aerospace Engineering. Executive MBA from IESE. Senior Engagement Manager at ALG specializing in ATM and Space.

system")